Retail competition for business customers will be a transformational change for the English water market, providing an enabler for customers to drive cost and water efficiency. The Market Blueprint consultation issued by the Open Water Programme in January 2014 sets out the programme’s recommendations for the high level design. Among other things, the Open Water Programme considers the establishment of a market operator to provide a range of market facilitation services to support the competitive retail market. These include registration and switching, financial settlement, data exchange and governance.

History has proven in many markets that the overriding theme is the absolute requirement for good governance. Get it wrong, and the arrangements could fail. Get it right, and the key decisions will be informed, engender stakeholder buy-in, and will deliver the desired outcomes.

The challenge for industry will be in the next phase of the programme, developing appropriate governance arrangements that balance the tension between accountability and responsibility while placing the correct incentives to spur competition.

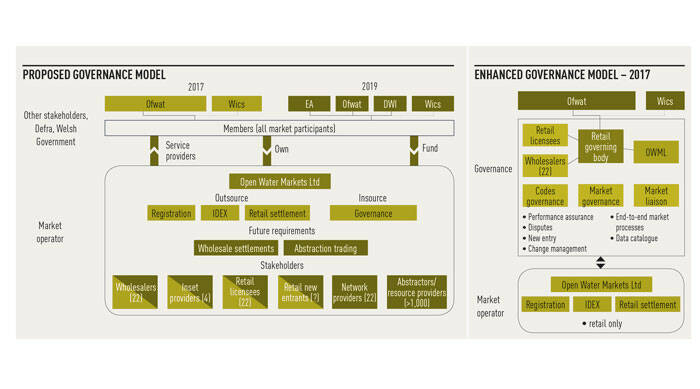

The proposals to establish a market operator are to be welcomed, and the arrangements being put in place to procure the central systems for registration, settlement and the industry data exchange. However, careful consideration needs to be given to the market operator ownership, commercial and governance models for 2017 so that it can facilitate the government’s wider aims for upstream competition. In particular, the governance proposals outlined in the blueprint feature a breadth of stakeholders like no other, involving wholesalers, retailers, inset providers, new entrants, network providers, and abstractors and resource providers (see Proposed governance model, below.)

The details of the governance arrangements have yet to be developed in full, but the breadth of the reforms and the mix of stakeholders mean that trying to govern both the retail and wholesale markets under one roof could be unmanageable and possibly a step too far.

The blueprint also considers a model where the IT and data services of registration, settlement and industry data exchange sit side-by-side with the governance services. In practice market arrangements could be further improved by providing for clear separation. Most recently, in 2013, the Department of Energy and Climate Change (Decc) introduced new arrangements that separated market IT facilitation services from governance for the national smart metering programme.

Within both the electricity and gas markets, retail governance arrangements and central IT services are provided separately. Conversely, the Scottish Water market features a single market operator (the Central Market Authority) providing retail governance services and central IT services, but this model does not currently feature any wholesale or upstream competition.

For separation to be effective, the correct incentives need to be placed on the parties to deliver the benefits. It is questionable whether a market operator, as outlined in the blueprint, that oversees large central IT systems is best placed to promote inclusive, accessible and effective consultation and administer arrangements in an objective, transparent and cost effective manner.

Indeed, building on this, the central IT facilitation arrangements in the electricity and gas markets have come under the spotlight over the past two to three years concerning whether such integrated business models (of delivery and governance) provide the industry with the necessary confidence in arrangements. This review continues.

Market separation must also apply independent challenge and rigour. Further separation, and indeed a physical split between the governance arrangement and the market operator, could facilitate a robust independent challenge of the market operator’s ongoing IT systems, costs and operations.

It makes sense to play to strengths. The separation of the (retail) governance arrangements from the market operator’s central services allows the market operator to be focused on security and the integrity of the central arrangements and services to market participants. System integration and ongoing IT service delivery are set to be integral functions of the market operator. However, the skills and expertise of IT management does not sit well with the unique skill sets of code management and secretariat services for market governance arrangements.

Market governance arrangements should be specific and proportionate to market needs. One size does not fit all. The governance arrangements must satisfy the principles of good governance and enable rigorous, independent challenge avoiding any potential conflicts of interest, whether real or perceived.

We can see merits for an enhanced model to have clear separation between the market operator responsibilities and the governance of the arrangements.

Drawing on experiences of other governance models, there is a case for further separation of governance from delivery. In other words, for the market operator to be focused on securing integrity of the central market systems and delivery of data services to the industry ( see Enhanced model, left).

As opposed to the market operator insourcing services for governance of the arrangements, this alternative model includes the establishment of a retail governing body that separates the retail governance arrangements from the procurement and operation of the IT systems. This retail governing body could provide the code administrative and support services for the retail and registration activities.

Having considered the contents of the blueprint in the context of the wider Water Bill and Water White Paper, we believe there are a number of options to allow a seamless evolution into the arrangements for upstream wholesale competition.

Paul Witton-Dauris, business development manager, Gemserv