European heads of state and government are planning to make a decision in October about whether to insist on a 40 per cent reduction in emissions levels by 2030, compared to 1990, on the way to its already stated commitment to near-complete decarbonisation by 2050.

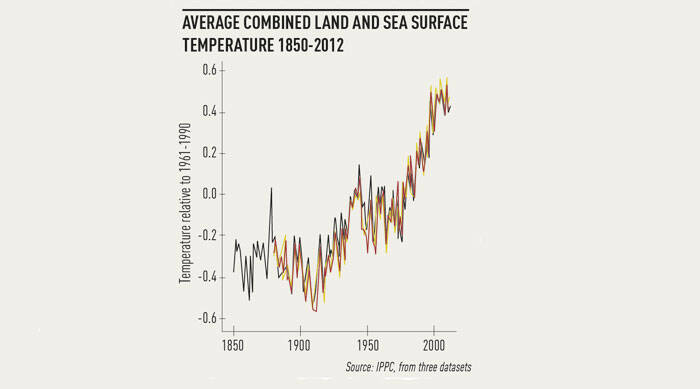

As the Intergovernmental Panel on Climate Change publishes a report setting out in detail the serious consequences for the world of climate change, why are we waiting that long? October is too late, even though it is only months away. Decisions are always slipping and we cannot afford to lose any more time, which happens again and again.

We need to kick-start the process for paying for this decarbonisation now. The European Climate Foundation estimates that a total investment of €7 trillion (£5.6 trillion) is needed for infrastructure if we are to decarbonise the European Union by 2050. This is the total number for the entire period until 2050. Because of lower fossil fuel costs and energy efficiency savings, among other savings, the average household would save €250 a year if this investment went ahead. While the total investment needed is significant, it is clear that governments and public sector banks will be unable to do it by themselves. Private sector money is needed but it is not flowing yet on the scale required.

According to Bloomberg New Energy Finance, investment in renewable energy dropped by 40 per cent in 2013, from $97.8 billion (£59 billion) to $57.8 billion – only partially explained by the lower costs of technologies such as solar panels and windfarms. While stable national policy frameworks exist in many countries, investors are still looking for a signal of high-level political commitment beyond 2020.

Apart from this current lack of a firm commitment beyond 2020, other obstacles to investment include:

• the weakness of the EU Emissions Trading System, particularly its inability to deal with large demand shocks;

• continuing disputes between member states and the Commission on state aid procedures and rules;

• the experience of retroactive changes to government incentives for renewable energy in countries such as Spain, which has increased perceived risk of similar measures in other countries.

However, there is hope. While the energy utilities, a traditional source of capital for energy investment, are in trouble across Europe and will not be providing the capital needed, there are others who can: institutional investors such as pension and insurance funds can fill that gap. They are in the position to provide the massive funding required. After all, institutional investors in Europe manage about €10 trillion.

Already, institutional investors are showing an interest in renewable energy. For example, Munich RE has made public its commitment to providing more than €2.5 billion for renewable energy. If Munich

RE is doing this, it is doing it for a reason: it understands that climate change is going to affect its business, because it is not prepared to take the risk of not acting against it. The Norwegian sovereign wealth fund is considering also directly investing in renewable energy. There are other pension funds and insurance companies around the world making the same decisions.

This is no surprise. There is a good match between institutional investors, who seek out stable returns over decades to respond to their pension and insurance liabilities, and the stable yield provided by low-carbon infrastructure such as renewable energy plants.

As investors, we can help fund Europe’s low-carbon transition. What we need are solutions to the obstacles outlined above:

• a clear and stable policy framework for 2030 with a greenhouse gas reduction target of at least 40 per cent;

• a reform of the EU Emissions Trading System that puts a meaningful price on carbon that can lead to abatement and that reduces volatility earlier than foreseen by the Commission;

• clarity on the future rules governing state aid and a resolution of ongoing disputes.

These policies will encourage people to take the risk and invest – and these policies will make more investments feasible. The longer we delay on those decisions, the more money is being lost or invested elsewhere, even in other low-carbon businesses elsewhere in the world.

Some countries say they need more time to analyse the impact on their country’s industry. We say, the time to act has come.

Investors will help provide the massive investment needed if EU heads of state and government adopt the right, ambitious framework. This will also bring other countries to the table and thus help offer a global response to climate change. The UN secretary general is starting a conversation this September that he hopes will lead to a binding global agreement on climate change in Paris in 2015, and hopefully reduce emissions so as to stay within the 2 degrees limit. This September deadline is going to be missed by the EU because while EU leaders are meeting to discuss it in June, they are not going to make the decision until October. This does not make sense. They have to make the decision earlier.