This week, Thames Water kicked off a 15-year programme to roll out smart meters across its area. It is starting in Bexley, southeast London, having completed successful trial streets there over the past two weeks and successful pilots to prove the broader business case over the past couple of years.

This is an industry first, for the Thames technology will surpass in functionality both traditional “dumb” manual-read meters and automated meter read (AMR) units. The latter have operational advantages in that they can be read more quickly and cheaply by operatives walking or driving by but they do not offer the near real-time data capabilities of fully smart meters.

Thames will roll out a fixed smart metering network, through which meter data will be transmitted regularly direct to its IT systems. This will give the company a near-to real-time view of water consumption, underpinning a range of operational benefits, including better leak detection, demand management and network visibility.

Customers will be able to access information on their consumption (hourly, daily or weekly as they wish) via an online portal, which Thames says could lead to a 12 per cent reduction in usage. The rollout will be accompanied by an extensive customer awareness programme and water efficiency device distribution.

Steve Plumb, head of metering at Thames Water, says the impact for both company and customer will be enormous. “It’s leading edge, it has to be said,” he comments. “It’s an industry first and the biggest customer-impacting project Thames has done.”

Plumb explains the move has been driven by a supply/demand imbalance that is “getting worse and worse”. He continues: “On a peak day in London, demand outstrips supply. By 2040, there will be a gap equivalent to the consumption needs of two million people.”

Smart metering was found to be the most cost-beneficial means of tackling the problem – driving down demand 12 per cent, providing visibility on network and customer-side leakage, and enabling the company to target mains renovation/replacement work where it is needed most. The programme is now a compulsory part of Thames’ Water Resource Management Plan, approved by the secretary of state in 2012.

A smart meter for every Thames customer will be delivered over three AMP periods and cost £300 million. Plumb notes the rollout “is not cost beneficial, but it is the least-cost option for tackling a water resource issue”.

So for Thames, smart meters are being driven by the need to solve a specific problem. Meanwhile, the demography of its patch – densely populated, particularly across London – will mean it can get a lot of bang for its buck with a fixed network. But what of other companies? Is smart metering a real option for them?

Beyond Thames?

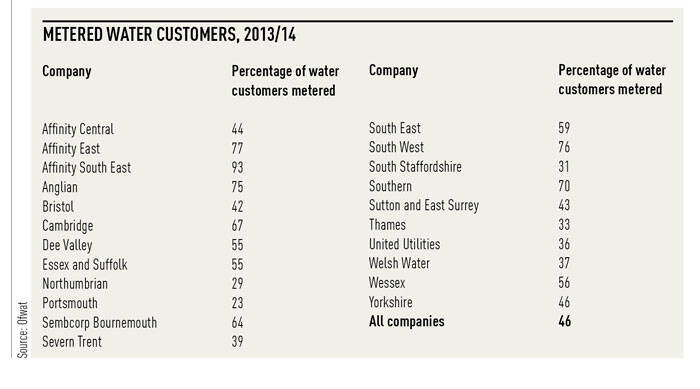

There is a mixed picture across the industry in terms of meter penetration, as the table shows. Understandably, the most concerted action has been taken by companies operating in areas of tight supply/demand balance.

Eric Woods, research director at Navigant Research, which late last year published a report on smart water networks, notes there is diversity in the industry, even within the ranks of the metered.

“There have been mixed approaches,” he says. “Some companies have got basic metering in first. Those who have gone for AMR tend to have been driven by operating costs, because they are cheaper to read. Once you have got a certain volume of meters, that’s just common sense.”

Woods adds that most new installations now tend to be of AMR units. Although these will not deliver the benefits Thames is seeking with near real-time data available to both customers and operational staff, they do offer operational advantages over traditional dumb models.

Southern Water is a good example of a company that has opted for AMR metering. It is more than halfway through a programme spanning AMP5 to universally roll out AMR meters, on water stress grounds. It is replacing 100,000 existing dumb units and installing 487,000 first-time meters. Chief customer officer and metering programme director Darren Bentham says the scheme is on track, with just shy of 500,000 meters in place so far and 230,000 customers moved off rateable value-based charges.

Bentham explains why Southern chose the AMR route over the fully smart option: “We wanted to do the whole thing in one AMP. We could make a good business case for drive-by AMR based on the whole life cost of running the asset. When we made our decision , the smart meter technologies available then were not up to it… we could not make a business case for a whole series of repeaters and collectors across the whole of our patch . They may have been okay in central Brighton, but not in more rural areas where meter density was lower.”

At 75 per cent, Anglian Water has a high meter penetration level – in part because it “started way back”, says Paul Glass, metering change manager. Once again, this was on water resource grounds. Although it has put in some 100,000 one-way radio meters since 2010, it also has “a big stock of ageing dumb meters”, explains Glass. It has been proactively replacing these since 2005, but hitherto the replacements have been dumb for dumb.

But Anglian now has upgrade in sight. “In AMP6, we are hoping to cross a very important rubicon,” says Glass, explaining that its PR14 business plan includes the proactive exchange of 800,000 dumb meters for AMR units. In part, this is because the technology has grown in sophistication and because the company has found “obvious benefit” from the 100,000 first-generation radio meters it has installed.

Obstacles

So while one-way AMR radio meters are starting to win favour over traditional dumb meters, excepting Thames Water, the industry has so far stopped short of taking the plunge with fully smart. The reasons are manifold. As noted, domestic metering of any sort is patchy and piecemeal and politicians have shown no will to mandate it – most recently by leaving metering policy out of the Water Bill.

In terms of smart metering specifically, a position paper from the SBWWI Smart Metering Suppliers’ Forum notes: “In sharp contrast to the energy sector, there is no mandate for smart metering for the water sector. Without this, and without a common focus, water companies have no shared vision of what smart metering solutions they would like to see in their future plans, and have not agreed a common specification for a smart metering system.”

Andy Godley, senior consultant at WRc, sees coordinated smart metering with water and energy as somewhat lost.

“Decc is pushing forward with energy smart metering,” he says. “The SMETS2 standard has no mention of water. Ofwat has more or less washed its hands of the whole thing and left it up to individual water companies… Its Smart Metering Advisory Group did at least pull people together. There is a need for debate, for a wider forum to look for agreement in terms of direction.”

Without a mandate and widespread buy-in, a further chicken-and-egg type problem is establishing a cost benefit case. Godley explains: “You need a density of meters to achieve a robust cost benefit case. But without universal metering, it is hard to build that density and hence hard to develop the cost benefit case.”

And again until smart meters hit the pavements, there will be little in the way of customer pull.

Interest swelling

Despite these obstacles, the picture is far from entirely negative. While Thames is the only company currently implementing a dedicated, universal rollout of AMI, many other companies are conducting or planning to conduct smart pilots and trials of one sort or another. David Green, business development director, smart metering, at communications network and services provider Arqiva, believes: “We are on the cusp of real AMI systems being deployed. I think many planned AMR projects will be replaced by AMI projects. We are talking to a number of companies about the possibilities.”

Dene Marshallsay, director of specialist water consultancy Artesia Consulting and chair of the SBWWI Smart Meter Suppliers’ Forum, concurs: “There is an enormous amount of interest in smart metering in the industry. Companies are coming at it a bit late in the current AMP – perhaps because they were waiting to see what would happen with energy smart metering – but momentum is gaining and many more are talking about investing or researching.”

Glass confirms Anglian “wants to do a fixed network trial during AMP6” to get a measure of how the sort of solution Thames is going for might work in its – often sparsely populated – geography. “There’s no one silver bullet here,” he says. “It’ll be horses for courses, company to company.”

Bentham says Southern too will be keeping an eye on “when is the right point to go to the next step ”. This, he says, will be strongly guided by the existence (or not) of customer appetite for more granular information than AMR can provide.

Drivers

Aside from maturing technologies, there are a number of drivers for the industry to start edging towards smart metering now. These include: growing strains on water resources; ageing infrastructure; brewing customer contempt for leakage; heightening service expectations from consumers; and the ongoing need to increase operating efficiency.

Deploying smart meters is an essential first step towards fully smart water networks, which would help water companies to manage all these challenges. This is because AMI networks can be used to connect other intelligent devices – for example, temperature/pressure sensors and district meters – enabling companies to continually detect leaks, control pressure and ultimately manage water balance in real time.

Moves towards smart meters and smart networks in the UK are also in line with global trends (see box).

Benefits

Migration to smart puts many potential benefits on the table for the water industry, its customers and the country. These include:

• More efficient operations: faster leak detection and repair; better fault finding; greater network visibility; enhanced supply/demand planning; and better capital investment/maintenance targeting.

• Customer service: Providing customers with clear, detailed information on their water usage and consumption patterns, enabling them to adjust their behaviour to save water, energy and money. More regular interaction with customers would also provide new relationship opportunities for companies.

• Environment: Lower consumption and reduced leakage enable reduced abstraction; this in turn cuts carbon emissions from water treatment and distribution processes.

• Resilience: reduced danger of demand outstripping supply.

• Flexibility: the frequency and extent of data collection are easily adjustable with AMI, facilitating short notice trials, ad hoc fault diagnosis and accurate customer query resolution.

• Affordability: granular consumption information could be used to inform social tariff design and entitlements to other hardship schemes.

Some of these benefits will be of particular interest to companies in water-stressed areas. Others, such as more efficient operation and improved customer service, will be of interest across the board.

Artesia’s Marshallsay comments: “It naturally falls to companies in water-stressed areas to take the lead. Metering is key to managing water resources… But there will be interest from others over time – trials are being planned by non-water-stressed companies too.”

Sensus marketing director Andy Slater concurs: “As networks move from AMR to smart, the cost benefit of AMI will start to work in favour of companies outside water-stressed areas… really lights up the whole network and potentially changes water company management capabilities from reactive to proactive. Companies currently work off a lot of assumptions; with smart, a lot of financial benefits flow from better network management and customer engagement.”

Thames’ Plumb even expects customer pull to develop over time. He says: “For us, it’s a pure water resources problem – metering is the best way of tackling that. But other companies may well ask, ‘should we be metering?’ After all, even if customers use the same amount of water, over 50 per cent of bills will go down. I expect customers will demand metering in the future. Particularly if you move from one area to another, you might well ask your new supplier, ‘why can’t I see what I’m using, like I used to?’.”

Smart technology choices

Before reaping any of these benefits, a water company moving to AMI will have to make a number of correct technical and operational choices. Aside from choosing the meter, they need to consider which communications infrastructure to use; which data services and analytic capabilities to deploy; and how much to invest in back-end IT systems.

Woods cautions: “They need to be clear about what benefits they want and what data they can use – whether their systems can handle it.”

A company whose main objective is to defer the capital cost of pipe replacement, for instance, would have different data, data collection frequency and IT system needs from one whose primary goal was improving customer service.

Thames Water is on the brink of making such decisions. It is in the process of procuring smart meters and communications infrastructure for the next 15 years, with contracts due to be awarded in May. Plumb says ideally Thames wants to deploy the same meter everywhere and while cost is of course important, “I want a technology that works”. He elaborates: “My number one priority is getting reliable and accurate data from the system. I have made a promise to customers about what we can give them and I want to keep it.”

There is a range of possibilities in terms of the meters and communications networks available. Plumb is “agnostic” about which is the right answer, but he is “looking for a supplier that is willing to put its neck on the block on connectivity and data quality”.

Communications network

The choice of communications infrastructure will therefore be vital for Thames and any other company that goes down the smart route. Water meters come with a range of practical considerations that in effect rule out some of the network options available.

Unlike energy smart meters, they have no mains power source, so they require a battery, and are most commonly sited in underground boxes beneath pavements or drives. This provides relatively easy access for maintenance or replacement purposes, while the location (at the boundary of the property) enables firms to monitor both customer-side and network leaks and faults. But the fact that meters are buried makes mobile network use, for instance, problematic.

Moreover, despite early optimism that smart water metering might be able to plug into the mandated rollout of energy smart meters, Decc’s choice of home area network communications has left water out in the cold: underground boundary meters are simply too remote to connect.

Some see this as a missed opportunity. Anglian’s Glass says he “looks with regret” at what’s happening in energy. “A smart rollout in water hasn’t been taken into account,” he says. “That would have been a smart thing for UK plc.”

Be that as it may, there are two main types of remaining network option that can fulfil the industry’s needs. Artesia’s Marshallsay describes these needs thus: “Water companies will want a network that will work on day one, that will pick up all of its meters, that will be reliable, secure and will deliver a certain level of service on data provision.”

The first type are mesh-style technologies, which rely on a large number of street-level data collectors and repeaters – for instance, mounted on lampposts and other street furniture. This type of network has been rolled out in parts of the US, where access to properties is relatively easy. While it has a relatively low capital cost, deployment can be slow, given the need to seek permission from multiple landlords and local authorities. Moreover, maintenance costs can be high, and unbudgeted costs resulting from delays and so on can easily creep up. The short-range nature of the communication can also lead to connectivity issues – for instance, if a meter is just out of range of the nearest collector or relay.

The second network option is long-range radio, where meters talk directly to a small number of communications towers. Sensus, a provider of one such licensed offering called FlexNet, says through UK trials with its partner Arqiva and large-scale deployment overseas, “we’ve shown how this single technology can communicate with meters in all locations, including water meters in underground pits”.

Arqiva’s Green argues long-range radio is reliable and yields greater net benefit than mesh technologies. “Long-range radio facilitates the transition to evolution of a smart water network because it can handle additional monitoring and control devices as they are added to the infrastructure over time.” In fact, he says: “a main driver to selecting a communications network is coverage of the water network as a whole, not just the endpoint meters at customers’ properties, particularly where the network transverses open areas”.

Less interested parties also have good things to say on the subject. Marshallsay calls long-range radio “a good solution”, while Woods agrees it has “a strong case”. Southern Water’s Bentham comments: “I see being the evolution for water metering where meter density is high and pavement collections are prevalent.” Anglian’s Glass speculates: “There could be a standard carrier for the country, perhaps – there are private wavebands that are reliable and have the right technical capability.”

Arqiva has already been selected to provide long-range radio in northern England and Scotland for the energy smart meter programme and could use this network to connect water meters. Smart water metering trials in central and southern England by Arqiva and Sensus show that the network could work for water companies nationwide.

Where next?

The water industry – initially led by those in resource-stressed areas – seems to be gradually ramping up its metering activities and laying the groundwork for future smart deployments. Progress is slow and steady, and in the absence of any kind of mandate, company-led. While WRc’s Godley is “frustrated by the rate of development”, he concedes, “I think it will happen”, citing a number of industry clusters pushing for it. These include the SBWWI forum, Water UK’s revenue metering group and WRc’s own smart meter user group.

According to Marshallsay, individual progress such as that being made by Thames Water will also have knock-on effects. He explains: “Once the benefits can start to be quantified, once the data analytics can really be quantified, I’m sure it will snowball from there. Companies are already actively discussing it with each other; they are moving forward in the next AMP . I expect lots of activity, trials and the sharing of benefits. I expect a much greater focus on smart metering in AMP7.”

While some are happy for water companies to be left with overall responsibility for developing metering in their areas, many feel some kind of cooperation would be helpful in at least developing a common agenda among like-minded stakeholders. This should include water companies outside water-stressed areas that want to take advantage of the operational and customer relationship benefits a smart water network can bring.

The SBWWI group calls for a National Smart Metering Forum, led by government and regulator, to include Defra, Ofwat, the Environment Agency, water companies, the supply chain and customers. It says this group could discuss policy to help the industry to plan ahead; agree common specifications; and improve cost benefit evidence to support the smart meter business case.

Marshallsay concludes: “All water companies are having to look at this on their own. There is no central leadership, unlike in energy. There is a danger that fragmented will not equal most efficient.”

He calls on Ofwat to fill the leadership vacuum, picking up its earlier good work on the now disbanded Smart Metering Advisory Group. This succeeded in getting stakeholders around the table to discuss the challenges and made useful contributions on the cost benefit case and data privacy/security issues.

“That work really needs to continue,” Marshallsay says, “especially as the cost benefit case evolves and more data starts to come back.”

Smart water world

Navigant forecasts the global smart water networks market will expand from an annual revenue of $1.1 billion in 2013 to more than $3.3 billion in 2022, at a compound annual growth rate of 12.8 per cent. Cumulative investment over that period is expected to total more than $20 billion.

According to Water 20/20, a report based on interviews and surveys with 183 global water utilities, conducted by metering specialist Sensus, smart water networks are capable of saving 25 billion m3 of water and could yield annual savings of up to $12.5 billion. The annual savings identified include: $4.6 billion from improved leakage and pressure management; $5.2 billion from dynamic asset management tools that enable optimised capital expenditure allocation; $2.1 billion from streamlining and automating network operations; and $600 million from automated water quality sampling and monitoring.