Last month Centrica chief executive Sam Laidlaw issued a stark warning on security of supply as Ofgem ordered a competition investigation into the energy sector. “We’ve already had five years of investment hiatus because of Electricity Market Reform,” he said. “We’ll then have a further two years of under-investment, and this is coming at a time when Britain’s energy security is being seriously challenged.”

Not everybody was convinced: the Daily Mirror ran his picture on its front page, headlined “The Blackout Blackmailer”. SSE’s Alistair Phillips-Davies urged the industry not to “scaremonger”.

However, Laidlaw has a point. The Competition and Markets Authority will report in 18 months, just as electricity capacity margins are set to fall to their lowest level this decade. The sector is under heavy political pressure to keep energy prices down, which will only intensify as we approach next year’s general election. The Energy Act has been passed, but much of the detail depends on secondary legislation that is still being worked through. Amid all this uncertainty, who will invest in keeping the lights on?

There is no doubt the market is getting tighter. Power stations are closing down faster than new generating sources are being built. Investment decisions are on hold as developers wait for the final details of the government’s Electricity Market Reform – and for Brussels to give its seal of approval.

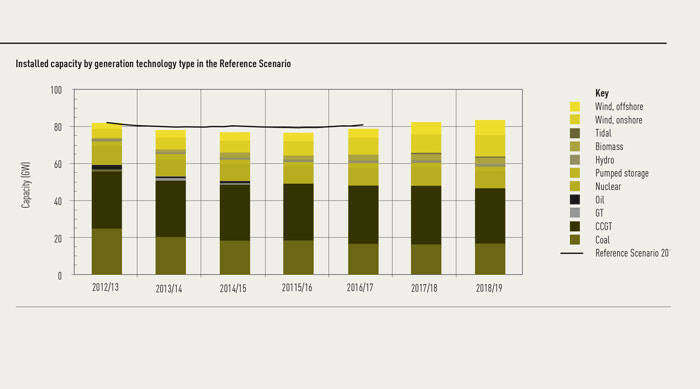

The capacity margin was around 15 per cent at the beginning of the decade, a comfortable buffer against unplanned outages or exceptional demand peaks. Ofgem, in its last capacity assessment in June, forecast a fall to just 4 per cent by winter 2015/16 (see ‘The capacity squeeze’, below). In the event of higher demand or lower supply, it could fall even lower, to 2 or 3 per cent. The worst case scenario presents a 1 in 4 chance of having to disconnect some customers.

There are some signs that the situation has deteriorated since June. Economic growth forecasts have risen, which tends to foreshadow an increase in energy demand. On the supply side, a hostile political atmosphere, tough economics and policy U-turns have put a dampener on investment. Two coal-to-biomass conversions have fallen away: RWE shut down its converted 750MW Tilbury power station and Eggborough is set to close 2GW by 2016 after failing to secure subsidies for a conversion programme. Several offshore windfarms have also been axed, although that is more of an issue for the longer term.

On the other hand, the Treasury’s carbon tax freeze could make it worthwhile for coal generators to keep running for longer. That is helpful for security of supply, albeit at the cost of higher carbon emissions.

The Department of Energy and Climate Change (Decc) is more sanguine than the regulator. By adjusting several of Ofgem’s assumptions, notably on demand and interconnection, it argues that the capacity margin will only drop to a safe 7 or 8 per cent. Decc is more optimistic about the take-up of energy efficiency measures and embedded renewable generation (which shows up as reduced demand). On interconnectors, Ofgem has conservatively assumed that we will make net exports of 750MW throughout winter, even when the system is under stress. Decc acknowledges that this is an uncertain area but suggests it is reasonable to expect zero net impact.

National Grid, as system operator, is not taking any chances and is assessing its options for reserve capacity (see picture caption on page 19). This could provide an opportunity for mothballed or unprofitable gas plant to be brought back online as back-up capacity. It is a sign of how dire the market is for gas generation that 7GW of operating plant has been put forward, as well as 2GW of mothballed plant.

Only a handful, if any, of those power stations will be awarded reserve contracts, however. The 4 per cent margin forecast under Ofgem’s Reference Scenario is just about enough to meet Decc’s reliability standard without extra measures. If we do see high demand, Decc estimates 300MW will be needed next winter and 1GW in 2015/16.

For the medium term, attention turns to the capacity market. Decc revealed final details of the design last month and developers are broadly satisfied that the 15-year contracts on offer will be bankable, but there are still significant risks.

Timing will be crucial. The first auction is scheduled for December, to bring on new gas plant by winter 2018/19.

Like everything in Electricity Market Reform, the capacity market is subject to state aid clearance from Brussels. If the European Commission raises objections, that could extend the investment hiatus and delay new generation for another winter. The Commission’s robust response to the UK’s planned support for Hinkley Point C nuclear power station suggests it is not inclined to wave everything through unchallenged.

While the Commission mulls it over, the government must decide how much capacity to procure through the market. Decc has set a reliability standard: demand must exceed supply, before intervention, no more than three hours in a year. It will not reveal until summer how many megawatts of capacity that equates to. That calculation depends on assumptions about all the other parts of the mix, which are themselves uncertain. If the government over-orders, consumers will pick up the tab. If the government under-orders, it will miss out on investment now and end up panic-buying down the line.

While the final market design appears to work for investors in new-build, the fate of existing gas plant hangs in the balance. Ironically, as developers are paid to bring new capacity on the system, even recently built gas power stations are at risk of closure as high gas prices hit profitability. The capacity market offers existing generators rolling one-year agreements. It remains to be seen whether that is enough to keep them on the system.

Meanwhile, there is huge uncertainty over the future of coal plant, which currently meets 40 per cent of UK demand. European legislation requires coal generators to meet tougher emissions standards if they are to stay on the system in the longer term. Under the capacity market, they can get contracts of up to three years to help boost the investment case for clean-up kit. The Treasury’s recently announced carbon tax freeze also favours coal generation. However, a lot will depend on changes in the coal, gas and carbon prices in the next two years.

There will also be chances for demand-side operators to bid into auctions in 2015 and 2016, but it is not yet clear what contribution this is expected to make.

Between National Grid’s reserves and the capacity market, it looks like blackout fears are overblown. Laidlaw was making a more nuanced point, that uncertainty will delay investment. Basic economics dictates that the tighter the market gets, the higher prices will go. One way or another, the consumer pays. As politicians fixate on energy prices, they cannot afford to ignore security.

What’s in and what’s out

Going off: Coal and oil

In 2009, there was 28GW of coal on the system. Some 8GW of that has already closed or will do so by the end of 2015, having opted out of the European Large Combustion Plant Directive (LCPD). The LCPD has also closed the last 3.6GW of oil-fired power capacity, which was expensive to run, polluting and rarely used.

The Industrial Emissions Directive will drive another round of closures. Generators have a choice: enter the UK’s Transitional National Plan or take up the Limited Life Derogation (LLD). In the first case, they must invest in kit to meet new emissions standards, convert to run on biomass or close down by 2020. In the second case, they may run for 17,500 hours or until the end of 2023 without upgrades.

At the moment, 9GW of coal is on the LLD list, but companies have two years to make a final decision and there could be changes. Confusingly, EDF Energy entered its West Burton and Cottam stations into the LLD but said it was exploring options to keep them open longer term.

Coal generators must decide whether the economics stack up to invest in life-extending upgrades. This decision will be heavily influenced by the carbon price. The Treasury’s recent decision to cap the UK carbon tax at £18 a tonne from 2016, instead of ramping it up, works in coal’s favour. It could mean more plant staying on. However, it is an increase on the £9 a tonne charged this year and remains a material consideration.

The current fleet of stations is four or five decades old. The older it gets, the more costly downtime and repairs they need to keep going.

Going off: Nuclear

There are currently nine working UK nuclear power stations, with a capacity of 9.2GW. The oldest of these, a 490MW Magnox reactor at Wylfa, is set to cease generating this year. Seven of the others are scheduled for decommissioning between 2018 and 2023, leaving only the 1.2GW Sizewell B. These dates are not set in stone, however, and owner EDF Energy may decide to keep them going longer.

Coming and going: Gas

As the government seeks to bring on investment in new gas power stations, some of the older stations are reaching retirement age. Others have been, or are likely to be, mothballed due to tough market conditions (see picture caption on page 19). High gas prices in recent years have made gas power generation uncompetitive against cheap coal.

There is only one gas-fired power station under construction at the moment – ESB’s 880MW Carrington plant. Other developers are waiting for the government’s promised capacity market to kick in before committing. Intergen is first in line with shovel-ready plans for two plants totalling 2.1GW.

In its Gas Strategy, published in December 2012, the government set its sights on 26GW of gas capacity by 2030. It is seen as a key part of the transition to a lower carbon mix, providing flexibility to back up intermittent renewables.

Coming and going: Biomass

Several coal generators have dabbled in biomass, first with co-firing and then wholesale conversion. While Drax is steaming ahead, others have run into difficulty. Ofgem forecast 2.5GW of biomass capacity coming from converted coal stations by 2016/17 and 1.4GW closing down. This 2.5GW replaces coal generation at slightly lower efficiency, so represents a small net loss of capacity. And some of it is in doubt: since Ofgem’s assessment, Eggborough missed out on conversion subsidies and looks likely to close by 2016.

Meanwhile, development of dedicated biomass has been all but halted after government got cold feet and axed subsidies.

Coming on: Wind

Renewable UK estimates there will be 10-11GW of onshore wind and 5-7GW of offshore wind on the system by March 2017. That is up from total installed capacity of 9GW today. Beyond that point, the picture is unclear as the old Renewables Obligation comes to an end and a new subsidy regime kicks in.

Ofgem’s assessment gives a more bullish, but not incompatible, total of more than 20GW by 2018/19. It considers 17 per cent of that to be “firm” capacity, which can be relied on to be available at any time. On average, wind turbines generate about a third of the time.