The last year could be considered one of two halves. On the one hand, the renewables sector continued to be buoyant and see specialist funds acquiring operating assets, while utilities and private developers recycled capital into new projects or used the proceeds to strengthen their balance sheets. Interest also remained strong in intermediary companies during the year.

On the other hand, deal activity in the traditional utilities sectors of water and thermal power generation was held back pending the outcomes of the PR14 review and capacity market auction, as well as continuing uncertainties over generation margins.

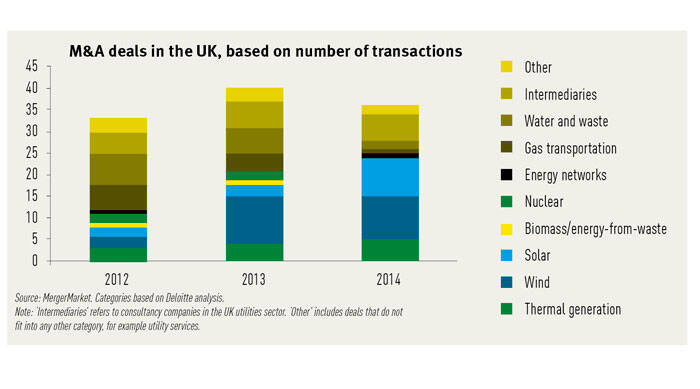

Our analysis is based on significant UK transactions in the generation (gas, hydro, coal), renewables (wind, solar and biomass), nuclear, water and waste, energy networks and intermediary sectors.

The number of UK merger and acquisition deals fell from 40 in 2013 to 36 in 2014 (year to 8 December). Fewer deals in the water and waste and energy networks sectors accounted for most of the decline, while there were no significant transactions in the biomass and energy-from-waste sector. With ten deals, wind continued to see the highest number of transactions, while the solar sector continued to strengthen with nine deals.

The average value of deals, where data was available, dropped more than 15 per cent between 2013 and 2014. Apart from healthy growth in the wind and solar sectors, nuclear was the only other sector where the value of transactions grew during the year, as Asian investors took stakes in new-build consortia. Smaller transactions rather than big ticket deals characterised 2014.

The renewables sector had a busy 2014. With 19 deals, compared with 2013’s 16, the sector accounted for more than half of transactions, both in terms of number and value.

Three offshore wind transactions made up three-quarters of the total value of renewables deals. Of the three deals, London Array 1 and Sheringham Shoal are operational Round 2 projects. Sheringham Shoal was the Green Investment Bank’s second acquisition of the year. The first saw it acquire 50 per cent of Westermost Rough with Japan’s Marubeni.

The sellers, some of them utilities, continued recycling capital into new projects during the year. However, Dong Energy’s sale of stakes in Westermost Rough and London Array 1 also represented a move to share construction risks, reduce debt and cut costs.

Interest in intermediary companies remained strong in 2014. These businesses engage in a wide spectrum of activities, including energy efficiency and monitoring services, demand aggregation, smart metering solutions and emergency generation.

With UK energy market trends regarding increased energy efficiency, intermittent renewable generation and peak demand management set to continue, intermediary companies will remain attractive to new investors.

The ongoing Electricity Market Reform and the lack of clarity on where clean spark and dark spreads are headed were the main drivers of uncertainty around thermal power plant valuations. While the number of thermal generation deals was up, deal values were smaller.

Clean dark spreads remained higher than clean spark spreads through 2014, leading to uncertainty over gas-fired power generation. However, there were signs of clean spark spreads improving during the year. This trend is likely to continue in the medium term with the expected reduction in coal generation as a result of the forthcoming increase in the carbon floor price.

Centrica’s announcement of plans to dispose of three gas plants, along with the results from the first capacity market auction in late December, could unlock appetite for generation transactions in 2015.

Compared with 2013, there was less apparent interest from Asian investors in the water sector as investors waited for Ofwat to finalise PR14. In nuclear, Toshiba acquired a majority stake in NuGeneration. China General Nuclear Power Corporation and China National Nuclear Corporation are still expected to invest in Hinkley Point C after the European Commission’s favourable ruling on European Union state aid rules. Subsequently, Hinkley Point C has also attracted interest from Saudi Electric.

Operating wind and solar assets will continue to offer relatively stable and predictable returns, and we can expect interest in them to continue. We may again see a number of solar deals this year as developers aim to finish development before April, when the Renewable Obligation scheme ends.

The results of the capacity market auction have brought some clarity, which may revive investor interest. In addition, UK water assets could become the centre of attention again following the finalisation of PR14.

James Leigh, partner, Andrew Durrant, partner and Dan Gambles, director, Deloitte