In recent months, there has been a changing of the guard at Centrica, with ex-BP director Iain Conn assuming the chief executive’s role.

And it is abundantly clear that not everything is rosy in the Centrica garden as last Thursday’s 2014 full-year results amply demonstrated.

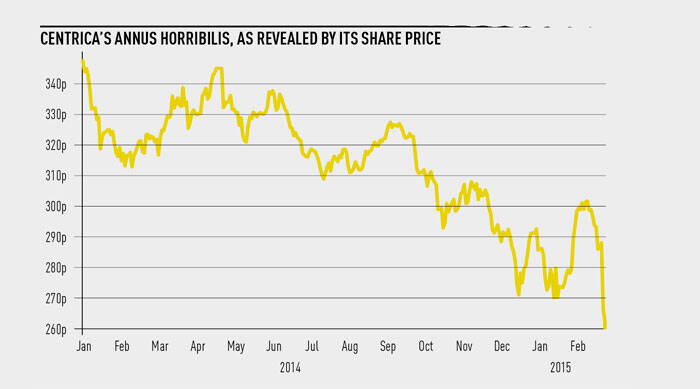

On the back of some decidedly poor – though not unexpected – numbers, Centrica’s shares fell by over 8 per cent on the day.

Investors have become increasingly concerned on three counts.

First, Centrica’s adjusted operating profit, at £1,746 million, was down 35 per cent compared with the £2,695 million achieved in 2013: the fall in adjusted earnings per share was somewhat lower at 28 per cent, partly because of a more beneficial tax rate.

Second, there was a dividend cut of 30 per cent, the first since Centrica was demerged from British Gas 18 years ago.

Third, on the back of the halving of oil prices in recent months, there were impairment charges of over £1.9 billion; these have effectively cut Centrica’s net asset value by a thumping 42 per cent.

All in all, 2014 was an annus horribilis for Centrica as an analysis of its underlying trading performance shows.

Of its £1,746 million of underlying operating profit, £823 million was attributable to its domestic British Gas business.

In 2014, operating profits from this market segment fell by 20 per cent, mainly because the weather was far warmer than average – never good news for Centrica, which thrives on lengthy periods of prolonged cold weather. Indeed, it sold about 20 per cent less gas in the UK last year than it did in 2013.

This business continues to be dragged through the political mill with leading politicians persistently agitating for price cuts.

In fact, domestic gas margins have already been cut. With the ongoing 5 per cent reduction in household prices, they would fall further if the Labour Party were in a position to impose its widely-publicised 20-month price freeze from next May.

Even more seriously under pressure is Centrica’s Energy division, which has consumed the lion’s share of investment funds in recent years.

Of course, with the Brent Crude oil price plunging from over $115 per barrel to below $60 per barrel in a matter of months, Centrica’s exposure to this development has been self-evident.

Indeed, Conn was splendidly laconic in pointing out that “we are stuck with $100 a barrel costs and $50 a barrel revenues”.

If the two figures were reversed, all would be fine and dandy. But the oil price is not expected to breach the $100 threshold again for some years, short of major international crises or an unexpected U-turn from swing producer Saudi Arabia.

Last year, Centrica’s exploration and production (E&P) returns were almost half those of 2013. And its E&P prospects for this year and for 2016 do not look that rosy either.

Neither is there good news for Centrica on its UK power station portfolio.

Its gas-fired plant segment reported another substantial operating loss of £120 million. It was slightly less disastrous than the 2013 £133 million loss, but that is hardly encouraging.

Such figures discourage potential investors that will help build the new gas-fired baseload capacity that is desperately needed; UK plant margins are now wafer-thin.

Furthermore, Centrica has confirmed the closure of its Brigg and Killingholme gas-fired plants, which were put up for sale last year.

Centrica also reported lower operating profits – £210 million against £250 million in 2013 – from its UK nuclear power station holdings with EdF.

In responding to these setbacks, Conn has not only cut the dividend by 30 per cent but also confirmed that capital expenditure will be cut by about £400 million over the next two years: Centrica’s net cash flow fell to just over £1.2 billion last year compared with almost £3 billion in 2013.

Even so, the increase in net debt – from £4.9 billion in December 2013 to £5.2 billion in December 2014 – was hardly excessive, although it was curbed by some material disposals.

Above all, though, Conn has presided over a 30 per cent slashing of the dividend, primarily on the pretext of preserving Centrica’s credit rating, which lies at the mercy of fluctuating energy prices.

For the longer term, he has set up a strategic review, which is due to report in the summer. By that time, prospects for the UK gas market may have become slightly clearer after the general election, which will inevitably highlight the Ed Miliband-inspired 20-month energy price freeze, to which Centrica and SSE are seriously exposed.

On the other hand, the uncertainty may endure, especially if the general election produces a hung parliament.

Thereafter, Centrica has other challenges to surmount.

First, the Competition and Markets Authority report – and whether a new government will implement its key recommendations – will loom large throughout 2015 and beyond.

Splitting up Centrica’s domestic gas business, which accounts for the overwhelming share of its 14.8 million UK customer base, may well be proposed.

Second, there remains the oil price. Its recent gyrations have defied the projections of most experts. Importantly, neither BP’s chief executive Bob Dudley nor his Shell counterpart, Ben van Beurden, expects a sustained recovery in oil prices for some time.

Theoretically, Centrica could spin off its E&P operations and seek to emulate mining giant Glencore with its Lonmin stake. Centrica could then return to being a high-yielding utility.

In fact, by grasping the dividend nettle, Conn has replicated the policy that Dave Lewis, Tesco’s new chief executive, has pursued. Both companies have dominated their respective sectors for years – and recently both have faced buffetings on several fronts.

Centrica’s dividend may grow again from a lower base, but yield-chasing investors will have noted that neither BP nor Shell cut their 2014 dividends despite plunging oil prices.

Undoubtedly, 2015 will be another challenging year for Centrica – it has already flagged lower underlying earnings. And they could be much lower than the market expects.

Nigel Hawkins, director, Nigel Hawkins Associates