In 2015, the number of merger and acquisition (M&A) deals in the power and utilities sector was broadly in line with previous years, despite some market uncertainty. The power generation M&A market was particularly affected by deals that were abandoned and others that took longer to execute. Although there were many transactions in the renewables sector, cuts in subsidies marked another step in the withdrawal of government support that may affect the number of deals in the future. In water, the completion of the PR14 review has so far had only a limited impact on the number of transactions. However, the agreement on Chinese investment is bringing much-needed certainty for the UK nuclear industry.

This analysis is based on UK M&A transactions in the thermal generation, renewables (wind, solar, hydro and biomass), nuclear, water and waste, energy networks and intermediary sectors.

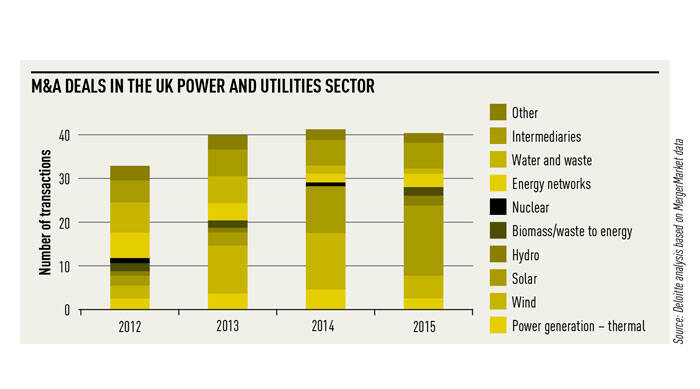

The number of UK M&A deals remained steady at 40 in 2015 compared with 41 in 2014 (year to 3 December). Significantly fewer deals in the wind and thermal power generation sectors were offset by a 60 per cent increase in solar deals, reaching 16 in 2015. There were two deals in hydro power generation last year (disposals by Infinis).

The average value of deals (where declared) increased by about 15 per cent in 2015. This was driven by larger wind transactions as well as the value of thermal power generation deals, which were unusually low in 2014. Again, there were no billion-pound deals during the year.

European coal and gas market developments over the past year continued to affect 2015 M&A activity in the UK. Coal-fired plants took advantage of falling coal prices until late 2013 with the clean dark spread (CDS) reaching a considerable premium over the clean spark spread (CSS). Since then, European wholesale gas prices have fallen as a result of the decline in oil prices and the carbon floor price has been increased to £18 a tonne, adding significantly to the cost of coal. These factors eroded the price advantage coal generation enjoyed over gas generation and, combined with emissions clean-up costs, are driving the closure of a number of coal-fired plants in the UK. The government wants new gas generation to come online, but CSS has not improved over the year and the investment case remains unattractive. This made deals particularly difficult and led to a number of transactions that started in 2014 being abandoned during 2015. No transactions in 2015 involved traditional power stations, and the three completed deals were in distributed and emergency power, with capacity market contracts providing extra impetus in this area.

The acquisition of operating assets by listed funds continued to drive M&A activity in solar and wind. In 2015, 16 operating solar assets changed hands compared with 10 the year before. The Foresight Solar Fund and NextEnergy Solar Fund bought 10 assets between them during the year.

The number of wind deals dropped from 13 to five, perhaps reflecting the impact of the lower number of expected assets incentivised by the Renewables Obligation.

As government reduces subsidies, investor and developer interest in building new solar and onshore wind assets is likely to diminish. As new development drops off, we are likely to see the future consolidation of assets in the hands of financial investors.

The water sector completed its latest five-yearly review in early 2015. Despite expectations that regulatory certainty would bring more M&A activity, Pennon Group’s acquisition of Bournemouth Water was the only transaction, representing the lowest number – and value – of transactions since 2012. However, there may be more M&A activity in the near future, particularly as existing companies and new entrants to the market position themselves for non-household retail competition from 2017. The fact that a number of water company stakes are held by closed-ended funds that will reach maturity over the next one to three years is also likely to drive increased deal volumes.

Interest in intermediary companies continued in 2015. This trend is here to stay because of UK market needs for increased energy efficiency and peak demand management. We will soon see transitional arrangement auctions, in which companies that provide demand side reduction will be able to participate in the UK capacity mechanism, providing a significant revenue opportunity to demand aggregators.

There are a number of processes that are live or have been announced – including National Grid’s sale of a majority stake in its gas distribution networks, the government selling down 70 per cent of Green Investment Bank, Arcapita’s planned disposal of Viridian, the sale of a 23 per cent stake in Southern Water by Australia’s Future Fund and the restructuring of RWE. All of which indicates that 2016 may be a busier year for M&A in the sector and may well give rise to the first billion-pound deal in four years.

James Leigh, Andrew Durrant and Dan Gambles, Deloitte.