Assuming that the Water Bill becomes law in its current form, from 2017 all non-domestic customers will have the opportunity to choose both their water and wastewater supplier. There will be increased co-ordination of the English, Scottish and Welsh non-domestic retail markets. For the first time, licensees in one market could be recognised to operate in other markets, allowing business customers to choose a single water and waste supplier across Great Britain for all their sites.

Moreover, the expected unbundling of the supply licence could allow new entrants into the retail market, potentially resulting in new suppliers, such as energy companies or other organisations with strong commodity retail experience. In addition, the competitive water market is likely to be served by intermediaries such as brokers, procurement advisers and potentially buying groups, which could dis-intermediate the customer relationship with the water retailer.

To better understand how the water retail market could evolve after 2017 we have looked at insights and lessons learnt from the non-domestic energy retail market and worked with large non-domestic water users to understand their needs and expectations from a competitive market.

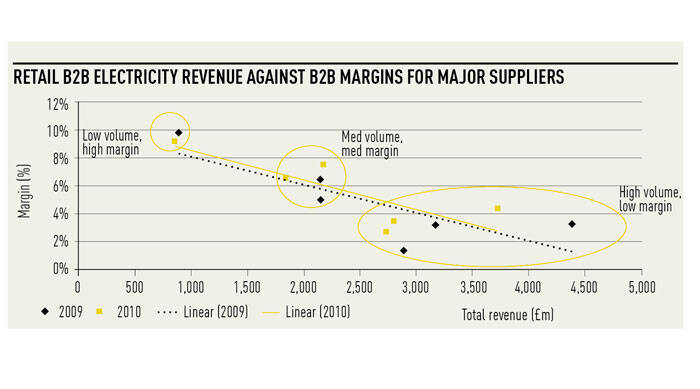

The first lesson is that scale does not translate into profitability. In the non-domestic energy retail market, the largest retailers (by revenue) report the lowest margins.

This can in part be explained by the effectiveness of certain customers (and their appointed third parties) in procuring energy, but it also reflects which segments of the market retailers have chosen to target and compete in.

The non-domestic energy market can be broadly understood in terms of three customer segments, each with differing needs, behaviours, and potential margins. The first is the SME (small and medium-sized enterprise) segment; the second comprises mid-market organisations; the third covers large multi-sites and high intensive customers. Almost all customers in the latter segment re-tender their supply contracts every 2-5 years and select a single supplier for all their sites across Britain.

While there are differences between the energy and water retail markets, we believe there will be many similarities as competition is introduced, especially in terms of customer expectations and behaviours.

An important lesson for water retailers is that they must be clear which markets they want to compete and operate in. The commercial strategy, operating model and capabilities required to win and be profitable in each of these market segments is likely to differ significantly.

For example, in the SME market, digital and proactive debt management capabilities are likely to be crucial in improving margins by managing cost to acquire, cost to serve and credit exposure. Whereas for large multi-site customers, effective data aggregation and analytics will be critical to provide customers with a single itemised bill across all sites, as well as helping to manage and reduce consumption over the lifetime of the water supply contract.

So what do large, multi-site customers expect from their chosen water retailer in a competitive market? Their top five expectations are: one supplier for all their sites, with a single point of contact; simplicity in service delivery, such as single tariffs across sites; transparency through regular reporting on an agreed standardised set of key performance indicators; empowerment, such as proactive warnings around irregular increases in water consumption; and confidence. In a market where there is no expectation for significant differences in prices between retailers, customers will make judgements based on their confidence in the water retailer to deliver on the outcomes promised.

Those water retailers who aim to win in a competitive market should be making significant investments in people, process and technology. They should start to make decisions on their commercial strategy now – in particular about where they will compete in 2017 and beyond.

We know from other competitive industries that “confidence” in their supplier to be able to deliver on their promises, is key in customer decision-making.