Uncertainties surrounding the impact of Electricity Market Reform (EMR) continued to make investors in the UK power and utilities sector cautious and drove a focus on operating assets last year. Our analysis shows that a key driver of mergers and acquisitions (M&A) activity in 2013 was the disposal of assets by utilities to recycle capital or bolster their balance sheets. With utilities taking a cautious approach to future investments, the UK has continued to attract Asian investors. Further, continuing uncertainty regarding natural gas prices has drawn a new class of financier, while market dynamics have led to the development of intermediary firms.

Our analysis is based on significant UK transactions in the generation (gas, hydro and coal bed methane); renewables (wind, solar and biomass); nuclear; water and waste; energy networks; and intermediary subsectors.

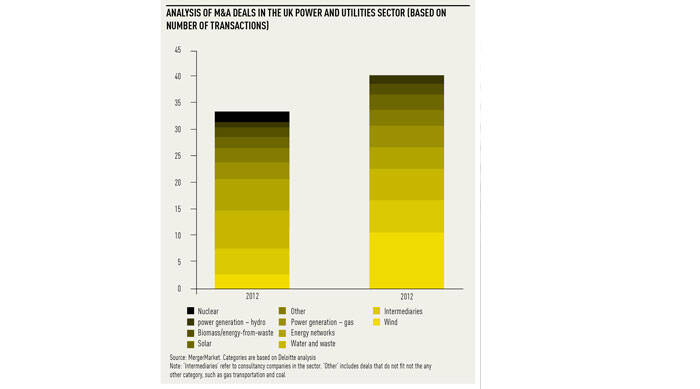

The number of UK M&A deals increased from 33 in 2012 to 40 in 2013. Most of this increase was down to the wind sector, where transactions more than trebled from three to 11. There were more solar and gas-fired generation deals and transactions associated with intermediary companies in 2013. However, the number of energy network and Ofto (offshore transmission) cables, water and waste transactions was lower. There were no nuclear deals.

In contrast, the total value of transactions, where data was available, dropped significantly in 2013. This was due to a handful of high-value deals in the previous year, including GDF Suez’s acquisition of the remaining stake in International Power, the sale of Wales and West to CKI and a financial consortium’s purchase of Veolia Water UK.

With 16 M&A deals, the renewables sector had a buoyant year. Some of these transactions related to the new trend of renewables investment funds listing on the London market. In 2013, four such funds raised approximately £850 million. Proceeds were mainly used to acquire operating onshore wind and solar assets, thus avoiding development and construction risks. For example, Greencoat UK Wind purchased six windfarms, the Renewables Infrastructure Group 14 onshore wind and four photovoltaic parks, and the Foresight Group acquired the Wymeswold solar plant. The Infinis listing was the fifth initial public offering during the year and reduced Terra Firma’s stake in the company to 69 per cent.

There was also increased M&A activity in the offshore wind sector. All Round One projects are now operational and a number of others are close to completion with investors becoming more comfortable with the specific risks, costs and technology requirements. With the renewable strike price and Ofto regime now providing greater certainty, assets are also becoming less judgemental to value. A number of offshore assets will come to market in 2014 as utilities focus on reducing debt or recycling capital from operational assets into development opportunities.

Asian investment flows

The sector continues to attract Asian investors. While Chinese investment dominated the Asian deals in previous years, there was growing activity from Japanese investors and interest from Singapore-based funds.

Asian investors view the maturity of the UK sector favourably, as well as the established regulatory and legal frameworks and its track record of accommodating foreign investors. Therefore, the UK is often viewed as a first step in expanding into continental Europe. This was a factor in Sumitomo’s acquisition of Sutton and East Surrey Water and is consistent with Osaka Gas’s strategy for subsequently acquiring half of that company.

Japanese companies have adopted a strategy of diversification and investment abroad, partly to combat economic headwinds at home, but also as a means of technology transfer. These factors underpinned Japanese investments in UK offshore wind generation and transmission. For example, Mitsubishi, as part of the Blue Transmission consortium, acquired the transmission assets of Sheringham Shoal and London Array.

The timing of the PR14 regulatory process may lead to a pause in Japanese interest in UK water. However, offshore wind – both assets and transmission – are expected to continue attracting investors in 2014.

There were no UK nuclear deals in 2013, but Toshiba announced the acquisition of a majority stake in NuGeneration, while China General Nuclear Power Corporation and China National Nuclear Corporation will buy substantial stakes in Hinkley Point C.

Wholesale natural gas prices continued to rise throughout 2013, supporting the price advantage of coal generation. For example, the Gas to Power Journal noted that clean dark spreads consistently outperformed spark spreads throughout 2013. This led a number of generators to reduce the capacity of their gas-fired stations. This trend is expected to continue in 2014 and could result in other gas-fired stations being mothballed or having their capacity reduced.

It is against this backdrop that UK gas-fired stations have attracted a new class of investor. In contrast to the typical owners (utilities or independent generators), gas plants were sold to private equity or pension funds. For example, Severn Power was acquired by a consortium headed by Macquarie’s Infrastructure and Real Assets division, and a 50 per cent stake in Marchwood Power by Meag Munich Ergo Asset Management.

The specifics of these deals vary. Severn Power represents the Macquarie consortium expecting future spark spread improvement. Vitol adopted a similar strategy when acquiring Immingham from Phillips 66, but it is also connected to Vitol’s upstream and trading operation. Marchwood is tolled and therefore reflects Meag’s longer-term stable cashflow requirements. These deals also reflect investors’ belief that the long-term UK outlook for gas generation will improve.

Intermediary companies

The past 12 months has also seen businesses emerge that complement the traditional utilities market. This trend reflects changes in the UK energy market, such as the increasing proportion of intermittent renewable power generation, energy efficiency and smart metering. These businesses engage in a wide range of activities including energy efficiency and monitoring services, demand aggregation and emergency power generators.

In 2013, six transactions were made in the intermediary sector, up from five in 2012. The seven-fold increase in deal value in 2013 was predominantly due to the buyout of Inenco by its management and Eon’s acquisition of Matrix Energy Solutions. With traditional utilities and regulators starting to take notice, interest in these companies will grow.

Most of the recent M&A trends identified here are expected to continue into 2014. Utilities will sell operating assets and there is already a pipeline of Asian deals for nuclear assets. Spark spreads are also likely to remain less attractive than dark spreads, which could lead to further gas-fired power plant sales. We therefore enter 2014 expecting a number of M&A opportunities across the spectrum of the UK power and utilities sector.