Reforming the beleaguered European Union carbon market has been on the climate policy table for so long that any hope of a swift solution has been long since abandoned. But over recent weeks Brussels has shown signs of a consensus approach to political intervention which could spark a recovery in carbon prices and change the way energy companies approach their long-term plans for the 2020s and beyond.

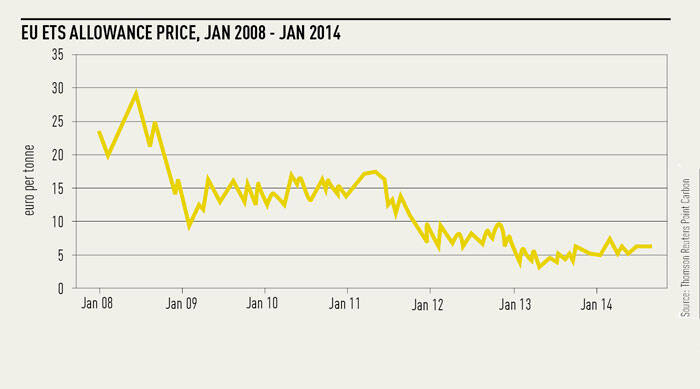

Since the economic collapse, the European Union Emissions Trading System (EU ETS) has staggered under the weight of a chronic and debilitating oversupply of emissions allowances because of lower than expected demand. The impact on the market has been to drive down carbon prices to levels that provide negligible investment signals to those interested in financing low carbon projects.

And while the EU ETS has become increasingly irrelevant, plans to curb the surplus by delaying the supply of further allowances to the market have proved divisive in the European Parliament.

Coal-fired power has therefore remained a strong source of profitable generation, while investment in low-carbon generation has been slow to come forward.

Now, however, with emissions backloading already in effect, the path towards implementing further reform is clearing to reveal a more promising prospect of market-driven investment in energy efficiency and low carbon technologies.

In short, the investment paradigm may finally be shifting in line with political will.

The position of EU member states on the proposed market stability reserve (MSR) is expected to be clarified by the European Parliament next week, with policy experts said to be optimistic that the plans for an MSR will be adopted more readily than the contested backloading reform.

In particular, Germany is understood to back a fast-track of the MSR plan, which the head of environment and sustainability at pan-European electricity group Eurelectric, Jesse Scott, says bodes well for negotiations.

Climate Change Capital’s head of policy, Martin Schoenberg, told Utility Week the timing of the MSR is the key issue of debate.

Schoenberg says the reform needs to come into effect in 2017 when the backloading of carbon allowances ends, rather than the proposed 2021, so that the carbon price can gain traction to deliver a market incentive by the 2020s.

The MSR would effectively manage the release of allowances back into the market following the so-called backloading plans and would need to be in place immediately after this to prevent undoing any market benefit, Scott explains.

“It would be ludicrous to backload to 2017, reload to 2021 and then bring in the MSR,” Scott says.

Another reason for a more timely implementation of the reforms is to hasten a shift in the way energy companies plan their long-term strategic investment, Schoenberg says. Positive implications could be felt for renewable energy, energy efficiency technology and the choice between coal and gas-fired power use, if the carbon market could be reformed.

“A healthy carbon price would reduce the cost of subsidising renewable energy and would provide an economic incentive for investment in energy efficiency,” Schoenberg explains. “In addition, the price signal would favour gas-fired power over coal-fired power, which would also reduce emissions.”

Taking the step to implement the needed changes should come sooner rather than later to provide a clear policy direction for energy companies looking to make long-term investment decisions and avoid the “carbon bubble”.

For example, a failure to show commitment to supporting carbon prices, and decarbonisation, could result in companies taking investment decisions on high carbon intensity generation capacity and running the risk of “asset stranding” once carbon offset prices rendered the investment uneconomic.

Schoenberg warns that even taking this regulatory step at an earlier date would require further intervention to reap the benefits. “The MSR is a very good step forward but in and of itself it will not be enough to boost carbon prices to where they need to be,” he says.

Currently, the carbon price hovers around €6 per metric tonne of carbon emitted, but most experts agree that a price above €40/mt is necessary to encourage switching from coal to gas, while proving a more economic case for investment in low-carbon technologies.

These price levels are only likely to become a reality within the 2020s, Schoenberg says. “It is quite far away,” he says, adding that investors should anticipate the change when planning their investment decisions to avoid a costly mistake.

“We definitely wouldn’t recommend investing into new coal plant,” he says.