The driving principle behind the Green Deal, the government’s flagship energy efficiency scheme was the “golden rule”. The promise was that you would save more over 25 years on your energy bills than the measures cost to install.

This was ingrained into the fabric of the Green Deal to protect future homeowners from taking on a property with onerous debt attached to it.

Now, the cast-iron guarantee looks set to be melted down and replaced.

Climate change minister and Green Deal champion Greg Barker has told the Energy and Climate Change select committee he wants the Green Deal to be “flexible” to allow people to install a wider range of (and more expensive) energy efficiency measures.

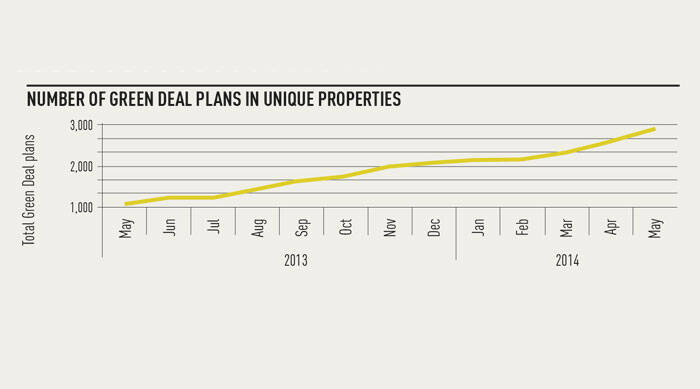

In its current form, the Green Deal finance package has not proved to be attractive to consumers. Of the 234,050 Green Deal assessments completed by the end of May this year, only 2,828 were translated into actual Green Deal plans.

Decc says that around 80 per cent of households assessed go on to install measures recommended by the assessment, but not under the Green Deal. They find other ways to fund the improvements.

This may be because, as Richard Twinn – policy and public affairs officer at the UK Green Building Council (UKGBC) – says, “the golden rule does provide something of a barrier to people taking up Green Deal finance”.

The issue is down to the projected savings of the energy efficiency measures and their cost to install. Some of the more expensive measures, such as solid wall insulation, may not recoup their costs over 25 years, while households installing multiple measures may also exceed their estimated benefits.

The answer being proposed to square the circle is a top-up loan. This would allow the eager energy efficiency aficionado to cover the cost of some of the measures installed via a Green Deal and then obtain a second loan – via the Green Deal framework – to cover the additional measures.

Barker said: won’t allow you to best the golden rule, but will allow you to do work in addition to but without encumbering the next purchaser of the property with payments that outstrip the savings.”

Decc has even had discussions with the Green Deal Finance Company (GDFC) about how a top-up loan system would work.

However, Twinn is not confident this would kick-start the flagging Green Deal. “If people want to install multiple measures, they are unlikely to be able to cover everything through Green Deal finance. They would, rather than arrange part of it to be financed through Green Deal and part of it through another loan, just do the whole amount through another loan,” he says.

Twinn adds that although top-up loans may encourage some households to remain within the Green Deal system, they are unlikely to make a significant difference.

The inclusion of feed-in tariff (FIT) and renewable heat incentive (RHI) payments in the calculations of the golden rule – something Barker says is a priority – “makes an awful lot of sense”, according to Twinn. This would mean FIT and RHI compatible measures – such as solar panels and heat pumps – could be funded via a Green Deal loan.

Jan Rosenow, energy consultant at Ricardo AEA, says these potential changes “go in the right direction” but there would have to be “a lot of other changes”. One of these would be legislative, because as it stands the golden rule does not factor in revenue generated, only savings made, and changing this “would be a little bit of a

difficult thing to do”.

Another tweak that could be made is to adjust the estimated energy savings of the measures installed. Currently, the laboratory-calculated saving of every measure is given a 25 per cent downgrade for its in situ savings. Mark Bayley, chief executive of the GDFC, says this needs to be re-examined and the measures that have been installed assessed “to see if that is too much of a discount”.

Twinn and Rosenow say another key area where Decc needs to look again is the interest rate. This currently stands at 6.96 per cent, which, Twinn says, “is a very competitive rate for what it does” but it “clearly isn’t attractive enough”.

He adds that reducing the rate to about 2 per cent would make the loan more attractive. He says cash behind the Green Deal Home Improvement Fund (GDHIF) could finance such a move.

However, the general consensus is that, regardless of what changes are made to the golden rule, the fundamental flaw in the Green Deal is lack of demand. However great a deal is, it makes little difference if nobody knows about it or wants to take it up anyway.

One way to address this apathy head on would be to make energy efficiency more financially appealing by, say, reducing council tax or stamp duty for energy efficient homes. Twinn holds up the car tax system as an exemplar of what can be accomplished: more fuel-efficient cars pay less in tax.

So, the golden rule is not quite as golden as we were led to believe, and changes of one sort or another are in the offing. But the real issue – as has been apparent since the beginning – is a lack of demand. The new golden (plated) rule – when it arrives – may make the Green Deal more attractive, but it could just be tweaking around the edges.