Across Europe, the decrease in available peak generation capacity is an escalating problem, as countries cope with mothballed gas-fired plants, nuclear phase-out and the integration of renewables into the energy mix.

However, while some issues are common to most or all European nations, it is national energy policy that often dictates how easy – or hard – it is for a country to mitigate the threat of blackouts.

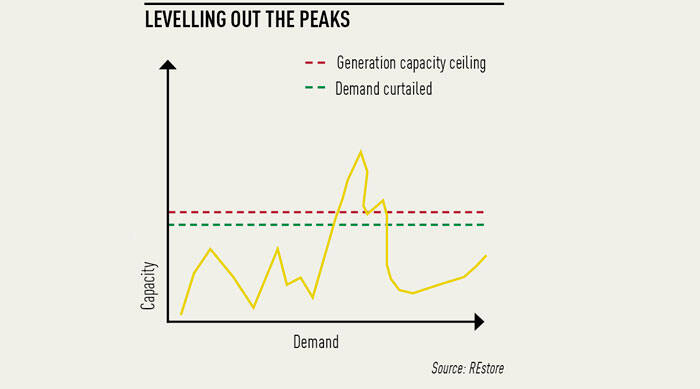

One option to alleviate supply and demand problems is demand-side response: reducing demand instead of increasing generation.

The US physicist Amory Lovins coined the term “negawatt” to convey this concept of energy management, and it is an apt way of describing the process of selling unused energy back to the grid at peak times.

The potential for demand response is considerable. In the UK, Ofgem estimated in 2012 that demand-side response could reduce peak demand on a winter weekday by up to 4.4GW. But selling negawatts is not always easy. The regulatory environment must create a level playing field for demand response operators and generators alike.

An an example of how to do this can be found in Belgium. Like Germany, Belgium is phasing out its nuclear power stations and at the same time is increasing renewable energy development. This puts additional pressure on the grid – so much so that Belgium’s energy minister recently voiced concern over the nation’s ability to meet demand over the coming winter.

His concern is well placed: there is a 1.2GW peak capacity gap looming over both this winter and winter 2015. However, the Belgian energy market is taking the right steps to rectify this situation by ensuring that the regulatory environment is negawatt-friendly.

Belgium’s capacity market allows demand response operators to bid for contracts with Elia, the Belgian transmission system operator, alongside gas-fired plants. The first auction was held in June this year, to secure 1.2GW for 2014/15 (to plug the aforementioned capacity gap).

The advantage of the Belgian capacity market is that it does not distinguish between energy that comes direct from generators, and demand-side response energy that ultimately comes from large industrial consumers. This level playing field has already paid dividends: the world’s largest steel manufacturer, Arcelor Mittal, has partnered with REstore in two of its Belgian factories to return 150MW to the grid.

By making it easy to participate in the capacity market, Belgium’s grid has access to the demand-response potential sitting within the nation’s biggest energy consumers – which, let us not forget, are often eager to join the capacity market because it represents a new stream of revenue.

In the UK, the first capacity market auction is scheduled for December this year, looking for 50.8GW to be delivered for 2018/19. Successful bidders will be required to provide peak capacity at times of stress on the electricity market, or face financial penalties.

However, unlike the Belgian capacity market, the UK is less favourable towards demand response – despite the potential noted by Ofgem back in 2012.

In Belgium, demand and generation are treated as equivalent technologies, delivering similar technical specifications and reliability. In the UK, there is no comparable equality between generation and demand, and they are treated differently.

For example, new generators are eligible for a 15-year capacity agreement, while demand response operators are only eligible for a one-year agreement. Demand response operators will only be able to compete for a capped 400-900MW volume. This assumes that demand response will contribute just 1 per cent of peak demand, with no prospect of this increasing any time soon, because generators will have a 15-year monopoly on capacity contracts.

In Belgium, there are no caps on the volume offered by demand response. All bids are ranked in the same merit order curve, and the cheapest bids are selected by the system operator regardless of the technology involved.

By creating a regulatory system that does not discriminate between demand response and generation, the Belgian market has increased its negawatt potential and made itself more attractive to big industrial consumers like Arcelor Mittal, which stand to gain from a system that makes itself easily accessible to demand response operators.

Any initial hostility to demand-side response from industrial consumers in the UK is born of concern that energy curtailment will damage day-to-day operations, or be more trouble than its worth. Once these corporations realise that it is possible to curtail power without affecting their industrial processes, they are always eager to participate in capacity markets.

Consumers need reassurance on two fronts: first, that demand response technology can unobtrusively segue into their operations; and second, that they will be rewarded for their efforts.

Aggregators’ technology is in place today to eradicate the former concern, but the latter depends on the regulatory environment. If demand response operators are going to be penalised simply because they provide negawatts rather than megawatts, nations such as the UK could lose their lights.

Pieter-Jan Mermans, co-founder of REstore