For PR14 Ofwat has implemented its new risk-based review (RBR) framework for assessing companies’ business plans. A key element of this is that companies whose plans are judged to be “enhanced” will receive a number of benefits, designed to help incentivise and reward high quality, customer-focused plans.

They will get: financial benefits (initial rewards and enhanced cost menus); reputational incentives (public recognition of high-quality plans); and early draft determinations (draft determinations by 30 April).

In addition, Ofwat has committed to a “do no harm” principle with regards to enhanced companies. This means that any changes in capital markets, which might affect the assessment of risk and reward, or any changes in policy or the assessment of new data, will be reflected in the determinations received by enhanced companies. This means they will not end up disadvantaged relative to companies that do not receive an early price determination.

On 10 March Ofwat announced the results of its initial RBR assessment of companies’ plans and determined that Affinity Water and South West Water had pre-qualified as being of enhanced status. Ofwat said South West had demonstrated a “strong focus on engagement and balancing the need to keep customers’ bills affordable”. Regarding Affinity, the regulator stated that both its “plan and company vision are innovative”.

While the reputational benefits associated with enhanced plans are intangible and subjective, the financial benefits can be quantified.

Ofwat has set out two financial benefits: an “initial reward” and an enhanced cost-sharing menu. In relation to the initial reward, the regulator has indicated that this can either be recovered in full during the 2015-20 period or added to the regulatory capital value and recovered over time. With regard to the potential upside from cost sharing, Ofwat has set an enhanced menu rate at 5 per cent above the standard menu (where the current assumption is that the standard menu has a sharing rate of 50 per cent, meaning that the enhanced rate is 55 per cent). Ofwat has specifically offered:

• for South West, an initial reward of £11 million and an estimated benefit of £6 million over PR14 arising from cost sharing.

• for Affinity, an initial reward of £4 million and an estimated benefit of £3.3 million over PR14 arising from cost sharing.

The value of the enhanced cost menu is uncertain. This is because Ofwat has not yet published its actual cost baselines or cost-sharing incentives for its standard menus. In addition, one cannot objectively determine whether a company’s “central expectation” would be one of outperformance against the menu (that is, the benefits published by Ofwat only arise if the companies outperform the baseline. If they do not, the enhanced cost sharing rate means they would incur a larger downside than had they not been enhanced).

For those pre-qualifying as enhanced, the estimated financial benefits can be secured only if they also accept Ofwat’s guidance on risk and rewards. This means they must commit to a wholesale vanilla weighted average cost of capital (Wacc) of 3.7 per cent, and retail margins of 1.0 per cent and 2.5 per cent in the household and non-household markets. In practice, both South West and Affinity chose to accept Ofwat’s guidance, and so confirmed their enhanced status. The question is, though, were they right to do so?

The answer depends on how much higher the returns might have been if they had challenged Ofwat at the Competition and Markets Authority (CMA), and their probability of success.

To analyse the trade-off more closely, we examined the published business plans of South West and Affinity and estimated the expected value they might receive from securing a wholesale Wacc above Ofwat’s indicated 3.7 per cent, and compared this with the lost value of rejecting their enhanced status (companies could also potentially secure higher retail margins via the CMA, but we have focused on the wholesale Wacc because it accounts for the vast majority of total value).

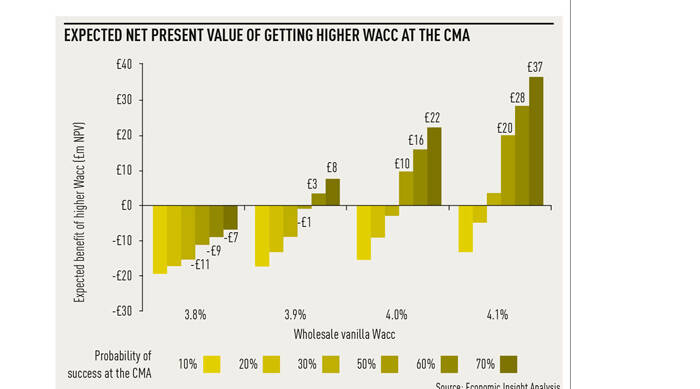

As the probability of securing a higher wholesale Wacc at the CMA is uncertain, we multiplied the benefit of this by an assumed probability, ranging from 10 to 70 per cent. Netted off against this was the 100 per cent certainty of surrendering the value benefit of being enhanced (losing the initial reward and cost-sharing benefit). The figures in the graph show the estimated value of securing a higher Wacc at the CMA, based on the combined data for Affinity and South West.

While the results are based on a number of assumptions (in particular, we have assumed that Ofwat’s assessment of the financial benefit arising from enhanced cost-sharing represents an appropriate central expectation), they do raise some interesting implications for South West and Affinity.

The first is that even if South West and Affinity had a high chance of success, increasing the wholesale Wacc to 3.8 per cent at the CMA is unlikely to be sufficient to offset the rejection of enhanced status.

The second is that the companies would need to have an expected probability of success of at least 60 per cent for an increase in the Wacc to 3.9 per cent to be sufficient to offset the value loss associated with losing their enhanced status.

Third, if the Wacc could be increased to 4.0 per cent, then a 50 per cent probability of success at the CMA would be sufficient to make rejecting enhanced status rational.

Finally, if a Wacc of 4.1 per cent could be secured, a 30 per cent probability of success would be enough warrant the rejection of enhanced status.

So the decision of South West and Affinity to accept Ofwat’s offer of enhanced status is consistent with them believing there was less than a 50:50 chance of securing a Wacc of 4.0 per cent or more at appeal.

For companies that have not pre-qualified, the trade-off of going to the CMA is, in a purely financial sense, less complex. For them the direct financial cost simply relates to the fees paid to legal advisers and external consultants, and the associated internal time costs. These costs can be traded-off against the benefits of securing higher returns from the CMA. In relation to the direct cost of going to the CMA, the government (as part of its consultation on streamlining the process for regulatory and competition law appeals) published an impact assessment in which it estimated the average cost of appealing a price control to be £320,000, with a high estimate of £800,000.

At face value, the low direct costs of appealing (relative to the potential benefit) might appear to give a strong incentive to appeal. However, in practice the trade-off is more complex, because issues such as the strength of the regulatory relationship and perceived external credibility – though more subjective – are also of importance.

Our analysis suggests Ofwat has broadly got the balance right in relation to the financial benefits from securing enhanced status in relation to South West and Affinity. In each case shareholders would need to be pretty confident of success at the CMA for the rejection of enhanced status to be commercially rational – and a single basis point increase in the wholesale Wacc would almost certainly be value-destroying even if they succeeded.

As this is the first time the RBR framework has been applied, there will almost be some lessons learned on both sides after PR14 has been concluded. For now, based on what is publicly known at least, Ofwat’s calibration of these incentives seems to be appropriate – as does the decision of South West and Affinity to accept the risk and reward guidance.