With the cliff-hanging Scottish referendum now resolved, politicos have turned to focus on the party conference season (Utility Week covers this week’s Conservative party conference on page 13). With voter concern about this winter’s energy bills high, energy will no doubt drive a deal of debate across the board, with a raft of differing views being expressed.

Labour leader Ed Miliband’s well-publicised price freeze pledge has already sparked some heated commentary, as has the prospect of the energy industry’s prodigious investment requirements for a secure future and the potential role of energy efficiency in easing demand.

Almost certainly, though, the party conference season will pass with a total absence of reasoned analysis about the “big numbers” that drive UK energy policy.

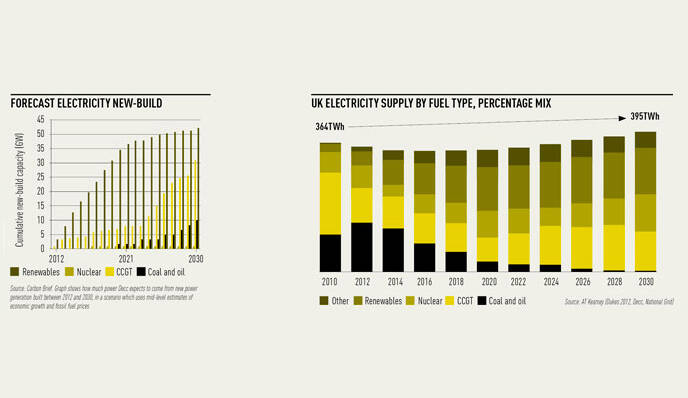

At its heart lies the 2010-20 investment programme, which entails a marked shift to green energy. The Department of Energy and Climate Change (Decc) has concluded that up to £100 billion still needs to be invested by 2020. Since 2010, investment has averaged £15 billion a year.

While some of the planned expenditure, including the ambitious offshore wind generation programme, has been pared back, the investment requirement remains very challenging.

Despite considerable expenditure being projected for enhanced transmission and distribution systems, much of the investment will be generation-related. Worryingly, within the investment projections, a modest amount has been set aside for new baseload plant, which is a vital determinant of plant margin – now below 5 per cent.

With two nuclear plants currently unavailable, there is very little margin left if demand should rise sharply or further unplanned outages occur.

Indeed, the only realistic baseload investment for the foreseeable future is the Hinkley Point C nuclear programme to build two 1,600MW reactors, which will not be commissioned until the early 2020s, assuming it gets approval from the European Commission for the 35-year £92.50/MWh inflation-linked price guarantee.

The £16 billion cost of this plant is unprecedented, even on a first-of-a-kind basis. It is way above the projected cost when nuclear new-build was being debated six years ago.

The construction of new gas-fired plant seems literally and metaphorically on the back-burner. Very low spark spreads have slashed returns from Combined Cycle Gas Turbine (CCGT) plants in recent years. Centrica’s £133 million loss on its CCGT fleet last year underlines the financial struggle faced by such plants. Moreover, it does not send positive signals to potential investors.

Despite the seemingly eternal quest to solve the emissions problem of coal-fired plant, nothing is immediately on the horizon because carbon capture and storage research has so far failed to produce scalable and commercially viable technology.

Interestingly, although new coal-fired plant has been built in recent years in Germany, its financial case has been assisted by low carbon emissions prices (see “Coal Generation Games”, Utility Week 19-25 September).

Much of the proposed UK investment expenditure until 2020 is related to renewable generation, despite its general inability to deliver baseload power.

To be sure, the combination of the recession, the lack of stable long-term renewable generation policies, political antagonism toward some onshore wind projects and the high costs of offshore wind development have dissuaded many potential private sector investors.

Nevertheless, the government has announced some large subsidies, both for offshore wind development, where current costs are around £150 per megawatt-hour, and for its stop-start biomass programme.

In the latter case, the UK’s largest power plant, the 3,960MW behemoth that is Drax, has been awarded generous price guarantees – of c£105/MWh – to convert one of its units to biomass fuelling. This figure is double the current wholesale electricity price.

While generation issues generally secure the headlines, investment in electricity and gas transmission is also formidable.

In total, it is expected that around £6 billion a year will be spent during the next decade as energy transmission and distribution networks – many built in the 1950s and 1960s – are modernised. Much of this investment will be undertaken by National Grid, the UK’s most valuable utility with a £34 billion market capitalisation.

Additional expenditure, of an estimated £11 billion, will be incurred to deliver the much-delayed – and controversial – smart meter programme, now due for completion in 2020.

Irrespective of the precise cost of the UK’s long-term energy investment programme, it is unquestionably formidable. Hence, it is salutary to consider how it will be financed.

The brunt of the cost will be borne by the big six integrated energy companies and National Grid. All seven of these companies, except Centrica, are highly-geared utilities. Their combined net debt currently stands at about £130 billion – no small sum.

Remember, too, that all these companies, and especially those based overseas, have serious concerns about the UK’s uncertain political environment.

Furthermore, Scotland’s SSE – having survived the Scottish referendum – has deferred decisions on certain major energy projects until after next May’s general election. Centrica, meanwhile, is selling – rather than building – gas-fired plants.

Politicians, therefore, expecting a post general election wall of money to be invested in modernising the UK’s creaking energy infrastructure, may well be sorely disappointed. Indeed, there are many sound reasons – unpredictable politics, the Competition and Markets Authority inquiry, low spark spreads, uncertain capacity credit remuneration and projected higher interest rates, to name just a few – for not investing in UK generation.

Finally, electricity and gas consumers have also been at the wrong end of the industry’s big numbers for too long. Since 1996, average domestic gas prices have effectively doubled in real terms while domestic electricity prices have also been driven up on the back of higher gas input costs.

A dual fuel bill currently averages more than £1,250 per household. No wonder the Miliband price pledge proved so astute politically, even if it has given an amber light to potential energy investors.

Many of these big numbers are overlooked by the media, which understandably focuses more on retail prices that directly impact their many millions of readers.

But this focus disregards the pertinence of industry’s investment numbers to the press’s favourite challenge of “keeping the lights on”.

Irrespective of what this year’s conference season throws up, there remains an abiding challenge for the utility sector to get this key message across effectively – all the more so given the complexity of electricity and gas finances.

Nigel Hawkins, director, Nigel Hawkins Associates