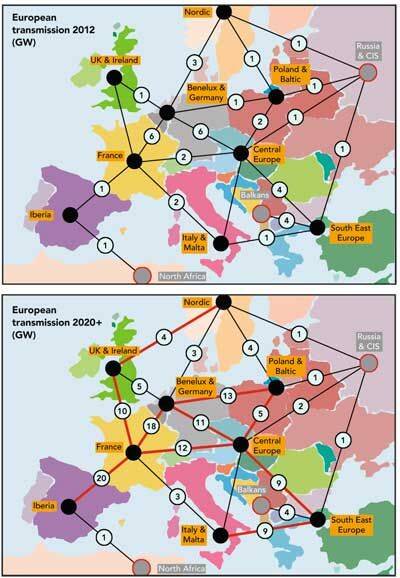

Achieving Europe’s 2020 renewables targets and legally binding decarbonisation goals at least cost is dependent on the greater integration of national energy markets. Integration relies on new transmission infrastructure that is able to support the trading of electricity between countries and connect renewable generation to centres of consumption.

The third package of European Union legislation was introduced in 2009 to enable this trans-national infrastructure and has already led to a series of framework guidelines and network codes designed to further liberalise energy markets in Europe and create a single market. But the vision of Europe in 2020 and beyond still requires a range of vital transmission investments between member states and with regions neighbouring the EU (see maps).

A number of practical steps and investment decisions have been made already, with transmission investments falling into three distinct but interrelated categories, each of which has a number of specific drivers affecting progress to date:

· Interconnection. There is currently a strong pipeline of interconnector projects, notably in the FUI region (France, UK and Ireland) and Germany (see table).

This is driven by: the opportunity created by the economic arbitrage between markets, which can be captured through additional interconnector capacity; providing a route to market for renewables; and inter-transmission system operator requirements to allow interconnected networks to operate safely.

· Offshore transmission. In offshore transmission, small-scale but nonetheless important investments in point-to-point connections in Britain, Germany and other countries have been delivered. These have focused mostly on connecting projects such as the potential 130GW or more of offshore wind due to be completed by 2030 in Europe. The challenge now will be in delivering the large projects.

· Large-scale reinforcement. The critical driver for investment in large reinforcement projects is the need to transmit power from higher resource potential generation areas to more densely populated areas of consumption. The importance of these projects in fulfilling the potential for renewable generation has already resulted in enhanced network investment incentives and a degree of technology innovation, while a number of large-scale projects have been proposed.

In addition to achieving a more interconnected and integrated market, a number of further benefits are expected. These include: enhanced security of supply through improved capacity and diversity; efficient price coupling and use of interconnector capacity through greater physical integration of markets; co-ordinated investment and planning; and greater market liquidity and competition.

A number of themes and challenges have emerged from the experience of developing such projects and from the interaction between investments. For instance, there is a need to co-ordinate investment in renewables and transmission to ensure priority access for renewables, security of supply and efficient, economic network investment. Competition must also be balanced with affordability to enable the best projects and attract developers and investors.

Moreover, renewable energy trading must be enabled via effective grid infrastructure, while liquidity must be pooled to increase integration. The economic regulation of transmission must be effective, and the trading of flexible generation, demand response and storage capacities must also be factored in.

The European energy industry needs to come together to explore realistic solutions to these challenges. The current regulatory, market and investment framework needs to evolve to deliver the required investment and, despite their different interests, all market participants, regulators and governments need to address at least the following five measures:

Regulatory framework for transmission. The sheer volume of exemptions under consideration suggests further revisions are necessary. Projects such as BritNed, EstLink, Imera and Arnoldstein-Tarvisio have all secured exemptions under differing criteria. However, questions remain as to whether a similar evolution is possible for merchant investment and what the acceptable trade-offs between risk and reward for the investor would be.

Structures to attract new sources of capital. The market as a whole needs to decide which finance structures would encourage institutional investors to the construction phase. Key questions include whether utilities are the only developers capable of underwriting construction risk, whether regulatory reform can change the risk-reward profile (as seen in the GB Offshore Transmission Owner regime), and whether traditional financing structures are adequate.

Innovative contract and risk management structures. The role of financial transmission rights (FTRs) is key in the development of market structures attractive to private investment. The market will need to establish whether FTRs provide an appropriate means to underpin merchant investment, priority access for renewables and the efficient allocation of costs, benefits and risks of co-ordinated transmission.

FTRs can help investors optimise returns and reduce the market risk from spot prices emerging from implicit auctions. However, using FTRs or other instruments to hedge exposures can produce a net reduction of earnings overall. The market will need to balance these inherent tensions.

Co-ordination in investment, planning and regulation. Efficient transmission network investment will increasingly serve multiple purposes, ranging from co-ordination between transmission reinforcements and interconnection, reinforcements and offshore wind connections, and offshore wind connections and interconnection. This will often require collaboration between member states.

Alternatively, where onshore or offshore reinforcement is triggered by new generation plant, co-ordination between transmission owners and generators is required. The challenges are therefore likely to be establishing who pays for the reinforcement, who co-ordinates it and whether anticipatory investment is required or has been made. Solutions could include risk-reward sharing, least regret expenditure and probabilistic assessment. No member state currently has a single transmission investment planning, co-ordination and regulatory framework able to address these issues.

Regulatory engagement and co-ordination. The current interconnector exemption process is long and intensive – often with a minimum 12-month timetable for initial stages of planning. There is plenty of scope for simplification or expedition.

The expertise and knowledge needed to develop truly interconnected electricity markets is in plentiful supply in Europe and the current barriers to success well understood. Industry participants must therefore come together to explore potential solutions to the stumbling blocks currently hindering progress.

Ilesh Patel is a director and David Balchin a senior consultant with Baringa Partners

This article first appeared in Utility Week’s print edition of 14th September 2012.

Get Utility Week’s expert news and comment – unique and indispensible – direct to your desk. Sign up for a trial subscription here: http://bit.ly/zzxQxx