Regulatory measures, including standards of conduct and tariff reform, are transforming the way energy companies are required to behave and engage with their customers. Smart metering and digital are creating new channels of customer interaction and new streams of data. Concurrently, consumer mistrust of suppliers continues to dominate energy headlines. This year’s July ICS Customer Satisfaction Index shows satisfaction in the utilities sector at its lowest level since 2010, and utilities as the UK’s lowest scoring sector overall.

This dynamic is creating a high risk and opportunity-rich environment in the UK energy market. The established companies now need to consider how they will embrace Retail Market Reform, fend off new entrants, respond to a new tariff structure and capitalise on a national smart meter rollout. To meet regulatory demands and achieve future growth, energy suppliers will need to invest in creating a low cost and high quality customer operation.

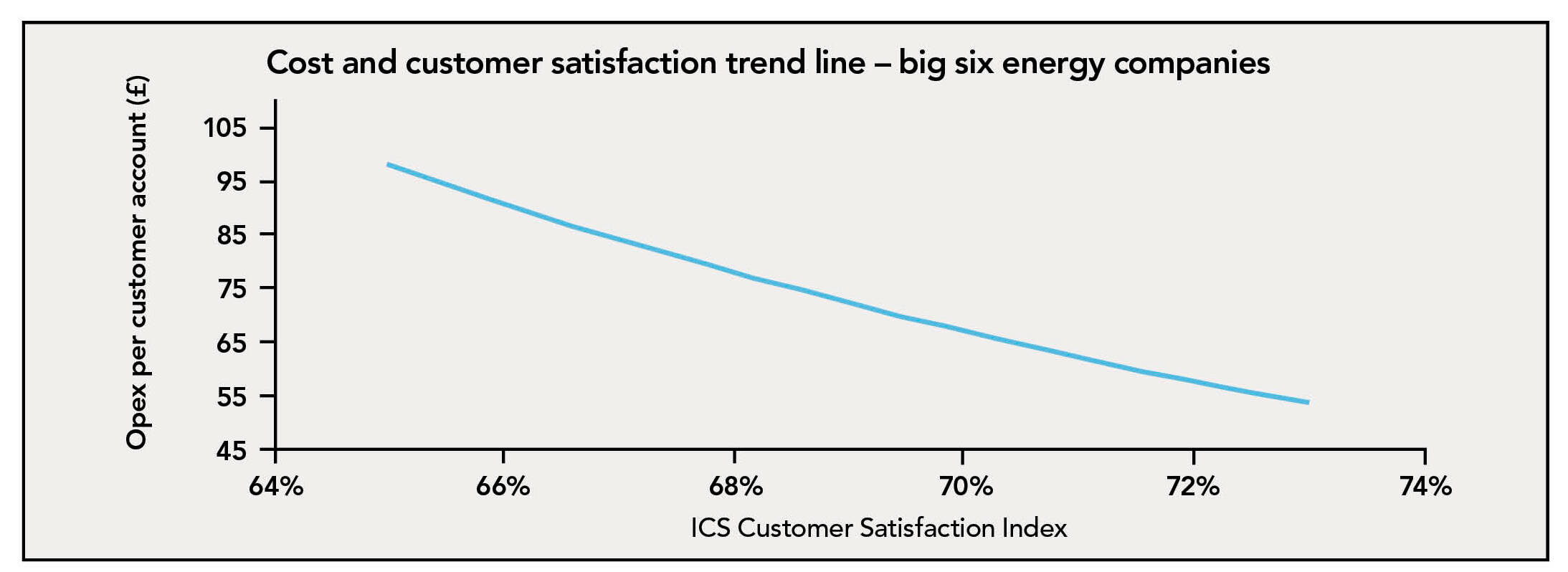

Traditional views on customer satisfaction hold that incremental improvements in customer service demand complex processes and premium systems that inflate operating cost. KPMG’s findings in the UK energy sector call this into question. We believe providing a great customer experience should lead to decreasing operating costs.

The analysis shown in the graph, based on the recently released 2012 Ofgem Segmental Reports, KPMG’s proprietary industry data and the corresponding National Customer Satisfaction Index, demonstrates that suppliers with the best customer satisfaction have the lowest cost base.

The data indicate a 1 per cent improvement in customer satisfaction typically generates a saving of £6 a year on the operating cost of a customer account. This represents a major opportunity for energy suppliers. Based on our analysis of the average cost to serve across the industry, a 1 per cent satisfaction improvement could lead to a saving of as much as 7.5 per cent of total operating expenditure. This would afford huge scope for savings that could be reinvested in customer service, digital capability and high impact smart propositions.

This is an unusual correlation and is not something we typically see in other industries. So why does it exist? In our analysis of organisations that fit into the more high-performing portion of this curve, we have found that they tend to have lean, “right first time” processes designed to meet customer expectations at every touch point. These organisations consistently deliver a higher quality, more considered customer experience. A failure to fully understand the customer perspective, on the other hand, typically results in investments misaligned to customer expectations. This invariably acts as a lead indicator of broken processes, poor data quality and compromised application functionality. The result of this is rework, manual intervention, inefficiency and low staff morale. This is a feature of the lower satisfaction, higher cost organisations we find towards the poor-performing end of the trend line.

Energy suppliers understand this relationship. But it is not easy to make the necessary changes. Data degrades and needs to be cleansed and kept clean. People need to be retrained and incentives realigned to meet standards of conduct and mitigate mis-selling risk. Processes need to be adapted and continually improved. Systems need to be updated and integrated to keep pace with smart technology, Energy Company Obligation commitments and rationalised tariffs.

So how do the high performers find an edge? How do they make the right investments while coping with unavoidable regulatory and technology change? It’s all about two key things: putting the customer at the heart of the operating model and making good commercial choices.

The first step in creating an operating model that delivers high quality, light touch customer engagement is to understand optimal customer experience. “Voice of the customer” analysis allows a company to listen to customer needs in the language of the consumer, and translate these needs into internal business requirements. Customer journey mapping provides a holistic picture of the end-to-end journey of a customer, and identifies the key “moments of truth” where business change can have the greatest impact.

As processes are redesigned to more closely meet customer needs, further savings can be driven out through lean process improvement. This methodology removes waste and enhances the value delivered from each business process. Savings are then reinvested at the key moments of truth, focusing on the areas that give the greatest experience benefit. This might mean, for example, rebalancing the sales team to focus on retention to minimise customer churn. Finally, the new customer processes are digitally enabled to support the shift to self-serve and light touch customer service channels.

Suppliers can typically realise further value by more effectively managing their customer portfolio. Understanding customer data is key to addressing commercial choices that may be driving excess cost and poor customer experiences. Smarter segmentation and insight generation from analytics can allow companies to better cater for customer needs. Understanding data enables more intelligent retention and acquisition activities. It also means that different segments can be more closely targeted to guide product and service decisions. Deriving this insight will become even more important as smart meters begin to provide actionable data sets that can inform business strategy.

Now is the time for suppliers to act on raising customer experience levels, not only as a regulatory imperative, but also as a value-enhancing mechanism. With price remaining a huge issue for consumers, and customer experience becoming increasingly important in the marketplace, it is critical that energy retailers seek to understand how the cost profile of their operating model affects the value they offer to customers.

By making operating model improvements and commercial decisions based on genuine customer insight, energy retailers can reduce costs while also delivering an excellent and differentiated level of customer experience. This is a key opportunity and will be the major competitive battleground over the next 18-24 months.

Simon Harvey and Alan Riley are with KPMG’s customer and growth team in the UK