When it comes to the affordability agenda dominating the utility sector, Ofwat is ahead of the curve. Jonson Cox raised concerns about water bills rising faster than average incomes from the start of his tenure as chair, in late 2012, long before Labour leader Ed Miliband took it into his head to promise an energy price freeze.

To get price cuts for consumers, Ofwat has made it increasingly clear to investors that they should expect lower returns in the next five-year period. It spelt out that message in January, with “risk and reward guidance” targeting a steep drop in allowed financing costs.

This makes the sector less attractive to investors and a survey published by Water UK last week shows just how concerned they are. It also reveals a divergence between equity investors in the publicly listed water companies and their counterparts at privately owned firms.

Indepen, which carried out the survey, solicited views from 129 investors, of whom 52 per cent responded. These included holders of equity in listed companies (Severn Trent, United Utilities and South West Water) and unlisted companies, bondholders, providers of long-term bank debt, ratings agencies and advisers.

The “risk and reward guidance” has made the sector less attractive or significantly less attractive to 94 per cent of unlisted equity holders, 86 per cent of bondholders and 85 per cent of advisers canvassed.

Under that guidance, the weighted average cost of capital (Wacc) allowance for the current price review (PR14) is 3.85 per cent, down from 5.1 per cent in the 2009 settlement. That is significantly lower than the 4.1 per cent to 4.9 per cent estimated in water companies’ draft business plans.

There will be greater scope for performance-related incentives and penalties over the next five years, however, which is intended to spur the industry to greater innovation and efficiency. If a water company exceeds expectations, it will be allowed to levy higher bills from customers as a reward. If it falls short, it will be hit in the pocket.

Equity holders in listed companies were more likely to see the upside, with an even split between positive and negative views.

Ofwat’s financeability guidance similarly got a pessimistic reception, with listed equity holders more upbeat than unlisted equity holders.

These concerns contributed to a deterioration in the UK water sector’s perceived attractiveness in comparison with other countries. Australia, the US and Canada are seen as better bets – but the UK remains ahead of eastern Europe.

Set against other UK sectors, water was viewed as less risky than electricity generation, energy supply and rail operations but as risky as or riskier than rail infrastructure, airports, telecoms and energy networks.

There were some positives for Ofwat. Most investors said engagement had improved, even if they did not always like the outcome. They were broadly positive or neutral about the effect of changes in PR14 on companies’ business plans.

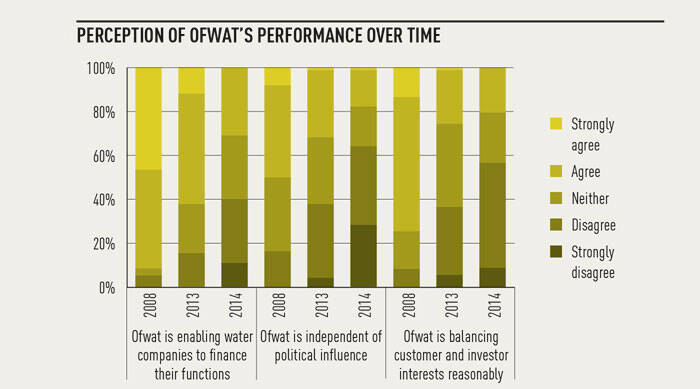

However, comparisons with previous surveys in 2008 and 2013 sound some warning notes for the regulator. Four out of ten disagree with the statement that Ofwat is meeting its statutory duty to allow efficient water companies to finance their functions. More than half say Ofwat has got the balance wrong between customers’ and investors’ interests, and six out of ten do not think it is independent of political influence.

An Ofwat spokesperson welcomed the survey, saying: “As we are currently in the middle of our price review, and as global returns diminish, we are not surprised to see a level of concern from some investors.”

Four companies have accepted the lower Wacc in exchange for fast-tracking, in the case of South West Water and Affinity Water, or earlier draft determinations, for Welsh Water and Northumbrian Water. Ofwat is set to publish draft determinations for the remaining companies in August.

The true test of Ofwat’s approach will be whether it prompts investors to quit the sector. There is little evidence of that so far. Share prices of the listed companies have risen in the past year: Severn Trent is up 12 per cent, United Utilities 22 per cent and Pennon (which owns South West Water and waste company Viridor) 16 per cent. As for mergers and acquisitions, no activity is expected until next year, after Ofwat has made final its determinations.

All the same, water companies cannot take investment for granted. At the same time as negotiating with Ofwat over their financial settlements, they are under pressure to reassure investors that they can perform well enough to bring in a decent return.