If you believe politicians, the UK can lead the world on any number of things. Recently, energy secretary Ed Davey has claimed just such leadership potential for shale gas (perhaps, if you don’t count the US), offshore wind (if we can crack our reliance on imported kit) and tackling climate change (never mind that UK emissions rose last year).

Carbon capture and storage (CCS) is another topic apt to put ministers in a jingoistic mood. Or was – it has gone a bit quiet lately. That is partly because the people behind the UK’s two leading projects are beavering away at detailed feasibility studies, not making announcements. It also reflects the fact that worldwide, CCS is turning out to be more difficult than expected.

As CCS Association chief executive Jeff Chapman puts it: “Energy ministers like to think that they are doing all sorts of leading the world on this or that, but if they look over their shoulder and no-one is behind them, they start slowing down a lot.”

In 2005, the G8 set out a grand but vague ambition to achieve “broad deployment” of CCS by 2020. That ambition has been battered by macroeconomic forces. In the US, cheap shale gas has displaced coal for power generation, cutting emissions far more painlessly than CCS could. It has also sent a glut of coal to Europe, which combined with a bottomed-out carbon price, makes it cheap to burn coal unabated. Add in a global recession, and CCS looks very expensive to cash-strapped national governments.

Kieron Stopforth, CCS analyst at Bloomberg New Energy Finance, is clear: “It is important not to be too optimistic about the future of CCS. The reality is that the cost of the technology is incredibly high.”

The global competition may have become more snail race than Formula One, but that does not mean there is nothing in it for the winner. With renewables and nuclear not exactly zooming into the distance either, the ability to cut the carbon emissions of fossil fuel generation still looks important.

There are eight operational projects worldwide, capturing carbon dioxide from industrial sources such as natural gas processing and fertiliser production. The power sector can learn some lessons from them on the transport and storage side, but it will need different technology for capturing emissions.

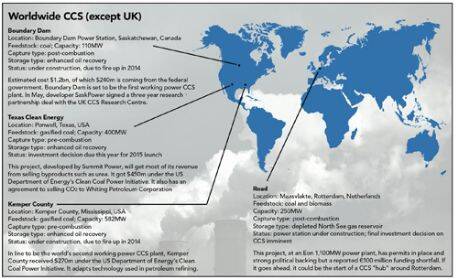

North America is leading the charge on CCS for power generation. Canada’s Boundary Dam project (see world map on page 24) is set to be first past the post. The Kemper County project, in Mississippi, is expected to be next in 2014. A third scheme, Texas Clean Power, could follow in 2015 if the investment case stacks up.

The UK sector has repeatedly failed to meet its own targets and has missed its chance for that world first, but can still claim to be leading Europe. Stopforth says: “The UK is definitely the frontrunner in Europe, not because the UK has done particularly well, but because everywhere else in Europe is so bad.”

The present government wrote in its 2010 coalition agreement: “We will continue public sector investment in carbon capture and storage (CCS) technology for four coal-fired power stations.”

Ministers failed to prevent the collapse of a £1 billion CCS competition launched by the previous administration, however. That was at least in part due to restrictions on the technology. Only post-combustion capture on coal power was eligible, limiting the pool. After five years, it came down to Scottish Power’s Longannet project. Chapman says: “It was 400MW of sparkling new CCS technology on the back of a very old 2GW power station. Scottish Power would have had to spend a whole lot of money to bring the power station up to modern standards to make it worthwhile fitting a fifth of its capacity with CCS, so they asked government for more money. Government said no.”

The competition was rebooted and opened up to other technologies. Two projects, White Rose and Peterhead (see UK map on page 23), have made the shortlist and are undergoing detailed feasibility studies. The £1 billion pot is not enough to fully fund both projects and they are expected to supplement the capital grant with a guaranteed power price through contracts for difference (CfDs). Industry is in closely-guarded negotiations with government over the terms of that support.

CfDs are a good way to support CCS, Stopforth says. “One of the problems with CCS is that it is so expensive, and the way that governments have tried to address that in the past is big capital grants… The CfD is helpful because it takes away the need for such big funding upfront and you can pay for the project over its lifetime.”

The support mechanism means three other projects are still in with a chance of being built. Chapman says: “The ones that weren’t shortlisted are hanging in there. They are not under active negotiation but there is nothing to stop them applying for support under contracts for difference.”

White Rose has also been entered for funding in the second phase of the European Commission’s NER300 programme – the only CCS project put forward. The programme was conceived to support around ten CCS projects from the proceeds of selling carbon allowances. Then the price of carbon plummeted, drastically shrinking the pot. Meanwhile, member states failed in the first phase to meet strict criteria for matched funding, with renewable schemes bagging the cash instead. “Spain, Germany, Poland, France, Italy… have more or less gone by the wayside now,” says Chapman. In the Netherlands, there are projects “struggling to stay alive” around Rotterdam.

Stephen Tindale, associate fellow of the Centre for European Reform, says that is a “major missed economic opportunity” for Europe. He is urging the Commission to find alternative sources of funding and make CCS compulsory for all new coal power stations.

For CCS to take off commercially, it must compete with other low carbon technologies, and that means slashing the cost. A CCS Cost Reduction Taskforce made up of academics, industry and government experts concluded that power generation with CCS could approach £100/MWh in the early 2020s. That would place it on a similar trajectory to offshore wind. However, projects must be built before the industry can learn and find those cost savings.

Stopforth is sceptical that this can happen without more financial support or regulatory intervention. He says: “There is a good chance there will be something in the UK, but there is no CCS revolution.”

This article first appeared in Utility Week’s print edition of 30th August July 2013.

Get Utility Week’s expert news and comment – unique and indispensible – direct to your desk. Sign up for a trial subscription here: http://bit.ly/zzxQxx