One might expect that saber-rattling from Europe’s largest supplier of natural gas would result in panic-buying and a steady price rally. But far from seeing pricing levels surge to record levels in line with increasingly threatening rhetoric from Russia, market players over recent months have been confronted with persistently bearish sentiment.

Currently, prices for prompt-delivered gas are languishing at the lowest levels seen in almost three years, while gas prices for this winter continue to slide despite shedding almost 14 per cent in value over the first quarter.

UK energy traders are unanimous: for now, a healthy supply-demand picture trumps the risk posed by a potential supply disruption from Russia this year.

“Prompt gas is currently at 31-month lows, reflecting how healthy storage stocks are after the exceptionally mild winter we’ve had,” says Icis European gas analyst Tom Marzec-Manser.

“In addition to this, we’re also seeing a very healthy supply picture. LNG deliveries are much more frequent as Asian prices seem to be easing.”

Market jitters over supply from Norway and the North Sea have also eased because producers have suffered relatively few unplanned outages recently. Scheduled outages are now made known to the market well in advance.

“People are able to better forecast with a lot more certainty going forward,” Marzec-Manser says.

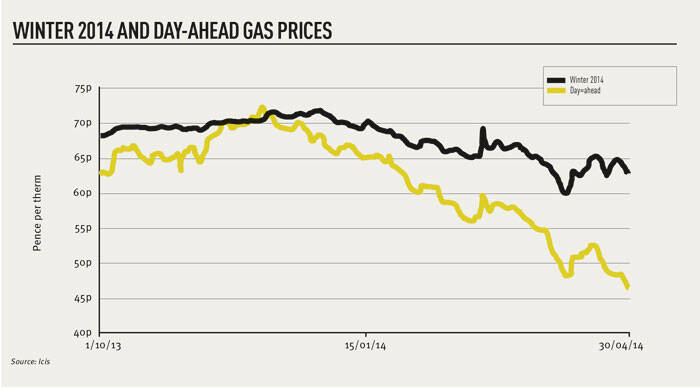

Icis, a price reporting agency, produces daily benchmark price references for the wholesale gas market. These show the winter value stubbornly above the 70 pence per therm mark late last year. This was driven by strong trading levels over the summer as the UK sought to replenish gas storage, which had been totally depleted over March 2013. By contrast, the most recent winter saw very little need to dip into storage, leaving the UK awash with gas and sending winter gas prices to lows of around 60p/th in April, Icis data shows.

Traders say that had the increased geopolitical tension surrounding Russia’s decision to annex Crimea from Ukraine not arisen, prices would have fallen further still. The “risk premium” helping to stem persistent losses could be around 10 per cent, traders say, adding that winter gas might otherwise have fallen to below 60p/th weeks ago.

“Even though the molecules which the UK trades and burns aren’t really sourced from Siberia, we’ve seen the NBP price rise as tensions with Russia increase, and fall back when some progress seems to be made,” Marzec-Manser says.

In the first weekend of March, Ukraine’s interim prime minister, Arseniy Yatsenyuk, told reporters that Russia had effectively declared war with a parliamentary vote approving president Valdimir Putin’s request to use force in Ukraine to protect Russian interests. Icis reports a Friday closing price of 64.95p/th and a Monday close of 69.35p/th following a 6 per cent hike over the day.

Marzec-Manser says that when a “reverse flow” supply agreement between Ukraine and Slovakia was agreed at the end of April, Icis saw the winter price fall from 65.10p/th to 64.25p/th, day on day.

Although not insignificant, Ukraine has diminishing importance as a gas transit route for Russian supplies. The greater diversity of transit routes is a result of a conscious drive on the part of European countries to build more links following severe disruption in 2009, which was also prompted by tensions between the two nations.

“The EU walked away from the 2009 event saying that there definitely needs to be greater interconnection within Europe to help reduce risk to security of supply, and there has been a lot of investment in that since then,” Marzec-Manser says.

A recent report from the Oxford Institute for Energy Studies (OIES) investigating the impact of the Ukraine crisis notes that Europe’s gas markets have less exposure to the risk of supply disruption because of the recent additions of Russian gas pipelines that skirt the borders of Ukraine en route to Europe.

“Because Russia supplies about 30 per cent of Europe’s natural gas and more than half of these volumes are still transported via Ukraine, issues of European gas security are raised,” the OIES says, “but Europe is in a better position to handle a potential disruption than it was on previous occasions.”

Before the building of new pipelines, Ukraine was responsible for the transit of 80 per cent of Russia’s gas supply to Europe, but this has been reduced to 50 per cent after the completion in 2012 of the Nord Stream pipeline, which carries gas from Russia to Germany via the Baltic Sea. Also relieving pressure on Ukraine is the Yamal-Europe pipeline, which carries gas from Russia to Germany via Belrus and Poland.

The OIES says much of the gas transiting Ukraine is destined for Italy – with supplies also going to Austria, Hungary, Bulgaria, Greece, former Yugoslavia and Turkey – meaning southeast Europe has the greatest exposure to risk.

“On the other hand these countries are in a somewhat better position compared with previous crises due to investments in new interconnectors and the adaption of existing pipelines able to work in a reverse-flow mode, typically from the Nord Stream pipeline in Germany down to Eastern Europe,” the report adds.

“There’s a relaxed feeling in the market that we might get by until autumn,” said senior gas editor William Powell in a webinar for market data provider Platts.

“Of course, there might then be very different fundamentals confronting the market. One shouldn’t be too complacent about this,” Powell added, pointing to the Dutch government’s recent decision to cut its domestic gas production with immediate effect. Gas supplier Gasterra will have to meets it contractual obligations through spot deliveries bought through the wholesale market, boosting demand.

Marzec-Manser says the impact of the Dutch production cut may already be reflected in wholesale market prices for gas, but agrees that near-term confidence could be shaken come the latter part of winter 2014-15.

“People are definitely relaxed about the supply picture through to the end of the calendar year. But it’s the end of winter – after storage stocks have already been depleted to some extent – that concerns over supply can arise,” he says .

Europe’s gas market players may well take comfort from current supply flexibility, but for a fair fight between bulls and bears 2014 may be too soon to tell.