The biggest question in a post-union world would be whether the single market continues between Scotland and the rest of the United Kingdom (rUK). Immediately after independence, the two side of the border would look the same. The Scottish government is likely to replicate the regulatory regime from rUK, with the same obligations on suppliers – at least initially.

One consultant told Utility Week that the business models of the foreign owned companies – EDF Energy (French), Eon, Npower (both German) and Scottish Power (Spanish) – already cater for supplying energy via a regional subsidiary. The creation of a new nation would only result in this business model being extended to the newly independent Scotland.

Stephen Hunt, analyst at UBS, says there are unlikely to be any significant changes should Scotland opt to go it alone and the single energy market continues. “I assume we will move to a 3 per cent retail margin across the whole of the UK, so from there, it’s not a massive downside if Scotland came out with, for example, a 2 per cent margin,” he says.

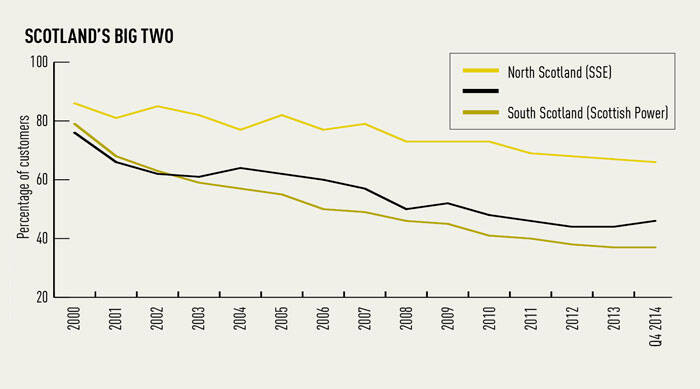

However, with the Scottish government eager for a single pan-utility regulator, differences could soon emerge. Scotland could end up with a big two, because the Scottish market is historically uncompetitive, with consumers there among the most unlikely in the UK to switch supplier.

Decc statistics reveal the incumbent suppliers – SSE (66 per cent) and Scottish Power (46 per cent) – have maintained a higher proportion of their historic customer base than the GB average (37 per cent) (see graph).

Coupled with the differences introduced as the two separate markets diverge – such as social responsibilities and the Scottish government’s focus on renewables, while rUK looks set to press ahead with new nuclear – the costs to serve the respective customers will also change. Decc estimates independence could add up to £189 to domestic energy bills for Scottish consumers, because the subsidy support for renewables would fall solely on customers in Scotland.

Tony Ward, head of power and utilities at EY, says that outside of energy, the currency adopted by Scotland will have the biggest impact. If Scotland was unable to continue with Sterling, then the introduction of a new currency and the associated exchange rate risk associated could drive some suppliers to exit the Scottish market. This extra risk, plus the doubling up of operational costs with additional customer service centres, could convince the other UK-based suppliers that staying in the smaller Scottish market no longer makes financial sense.

Ward adds: “It is the broader stuff – the regulation, the legislation – that will largely determine the overall outcomes here. Retail will be a consequence of the lot of it.”

Scotland special part 1: The last days of the union?

Scotland special part 2: Ed Davey and Fergus Ewing

Scotland special part 3: Untangling energy will be no easy task