As Ofwat drives separation between retail and wholesale businesses, water companies must grapple with a more complicated system of allocating customer performance accountability without any official guidance. Companies must create clear commercial arrangements that account for the customer measures in order to avoid millions of pounds in financial penalties.

Ofwat recently agreed to keep its service incentive mechanism (SIM) largely the same for the next regulatory period, 2015-20. However, within the same period the regulator is pushing on with wholesale-retail separation.

These changes will leave retailers and wholesalers to sort out the allocation of penalties for retail customer frustration about wholesale issues, such as leaks, supply interruptions and low pressure. Water companies will need to determine how best to arrange this internal contracting between their retail and wholesale businesses.

The SIM framework has successfully driven up the quality of customer service since Ofwat introduced it in 2010. According to data from Ofwat and the Consumer Council for Water (CCWater), customer satisfaction has significantly increased, with written complaints down 20 per cent and customer contact satisfaction increasing from 4.1 out of 5 to 4.4 out of 5.

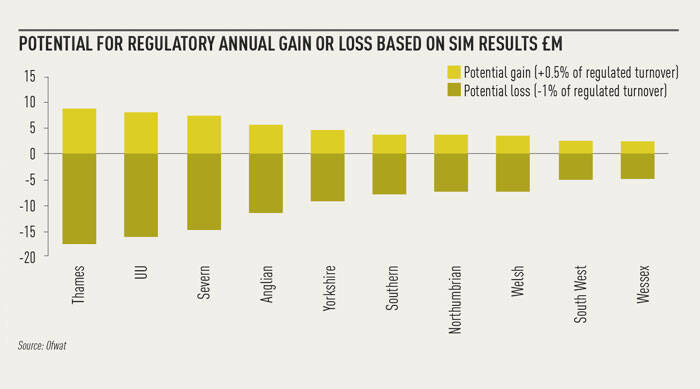

A central feature of the SIM framework is the financial incentive for good customer performance and significant revenue reduction for poor performance. The average water and sewerage company can lose up to £37 million because of poor customer service. The largest water utility, Thames Water, has the potential to lose £17 million in one year and more than £80 million during a five-year regulatory period.

After a detailed industry consultation on the future of the SIM, Ofwat agreed to minimal changes to the framework design and application of price controls. The framework will be similar in structure and form to the current incentive, but with more weight given to a qualitative assessment of customer performance. (Qualitative will be 75 per cent and quantitative 25 per cent.) The symmetry and magnitude of the financial incentives and reductions will remain the same.

Even so, the impending separation between wholesale and retail businesses will affect how water companies manage within the framework in the future. The separation of businesses will result in an extended supply chain across the whole water and waste process.

This supply chain will include the retailer and wholesaler and contractors on both sides, such as outsourced call centres and meter installation services. This structure means retailers will likely receive customer feedback for some services controlled by the wholesaler. As the retailers will be subject to the SIM measures and financial implications, they will need to contract with their wholesale counterparties to share accountability by passing on the some incentive and financial risk.

There are clear areas of overlap in the extended supply chain, such as accountability for customer complaints and abandoned calls. Water companies have two options to apportion the benefits, risks, and costs across the extended supply chain.

Option 1. If retail and wholesale businesses decide to share and apportion responsibility for unsatisfactory customer service, this will drive a more collaborative service across the supply chain. However, sharing accountability and financial exposure is difficult among multiple parties and is likely to increase the number of disputes and management time.

Option 2. The extended supply chain may be too complicated to share customer service performance responsibility. Water firms will need to price contracts so that only one part of the business is totally accountable for success or failure in the SIM. This option is easier to manage but will be costly for one side or another if the risk is priced incorrectly.

In either situation, strengths and weaknesses will be exposed. Water companies should try to collaborate effectively with partners and assign accountabilities to those who are best placed to influence the outcomes. Deciding a fair allocation of accountabilities, mutually beneficial partnership agreements, and a transparent approach to monitoring performance, will be key.

Contract management will grow as an area of significant potential value. Therefore, it is important for water companies and major contractors to consider their operating models, capabilities, and processes to manage this complex new environment.

There is a real opportunity for the whole supply chain to improve the customer experience and benefit from the SIM incentives. However, if water firms fail to build a robust line of sight from retail to wholesale and through the supply chain, the risks increase.

Dan Mitchell and Tim Wright, Oliver Wyman Utilities & Energy Practice