In January RWE announced plans to close seven UK power plants by 2023, while SSE announced plans to close a further two plants over the same time span. EDF effectively deferred a decision to commit to the long-term operation of some of its major power stations and Eggborough has indicated an uncertain future for its Yorkshire power station.

The large number of power stations already closed in the UK, together will those pending, equates to approximately 18 per cent of peak demand requirements.

It has been 40 years since Britain built its last coal-fired plant, and despite contributing 41 per cent of electricity generation in 2013, the average age of Britain’s coal fleet is now 46 years. Meanwhile, Britain’s nuclear fleet, which contributed a further 21 per cent of generation in 2013 (bringing the combined share up to 62 per cent), has been generating for an average of 32 years and must be almost entirely decommissioned within a decade.

By contrast, Germany’s newest coal power station is barely a month old and, with a conversion efficiency of almost 46 per cent, could be using as much as 25 per cent less coal than Britain’s oldest coal-fired plants while creating fewer harmful emissions in the process.

It seems unlikely that Britain will opt to build new coal-fired power stations as Germany has done, but over the next decade this ageing fleet of power stations is likely to create numerous problems for a country whose current nuclear fleet will consist of just one power plant from 2024, Sizewell B, and that is due to be decommissioned in 2035.

A big driver of coal plant closure has been the Large Combustion Plant Directive, coupled with the carbon floor price. The directive mandated that coal plants either meet emissions standards or close by 2015 or close after 20,000 hours of generation (whichever came soonest). The decreased revenue for coal power stations running on the 20,000-hour regime caused by the introduction of the UK carbon floor price in April 2013 led to them accelerating use of these hours, with a number of them shutting prior to April 2013.

Between this directive and the carbon floor price the result has been the loss of 9.6GW of capacity in 2012 and 2013, with a further 3.9GW expected to go by 2015. Further closures might be expected in 2015 as Eggborough, which can continue to operate under the Large Combustion Plant Directive, may opt to shut down if it is unable to secure financial support for biomass conversion.

A second directive, the Industrial Emissions Directive (IED), will further reduce the number of old coal and gas-fired plants. The loss of these ageing plants is perhaps inevitable, but by 2023 EnAppSys estimates that under a scenario of high carbon prices, the closure of coal-fired plants under the IED could amount to as much as 12.5GW, with combined coal and nuclear capacity potentially falling by as much as 75 per cent from 37.5GW in 2013 to 9.4GW in 20235.

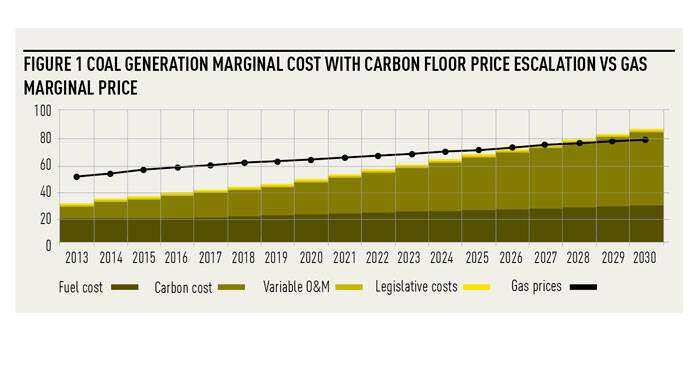

The graph shows a projected future cost per megawatt-hour of coal-fired generation, including the current carbon floor price escalation charges, with the equivalent figure for gas plotted on the same scale. It shows the squeeze on profits at coal plant against increased capital costs for upgrading to meet the IED, and shows why those coal stations that do not intend to or cannot switch to biomass are considering closure.

Current UK policy is to seek further growth of renewables, and to build new nuclear and conventional capacity, and to encourage gas-fired generation to remain operational. This is being achieved through tax support on shale gas, the introduction of a generation capacity mechanism and price support for renewables (the latter two via the Electricity Market Reform Bill).

While renewable price support (contracts for difference) is likely to lead to renewables providing increasing volumes of generation over the next decade, much of its output will be intermittent. Storage technologies could provide a solution, but the government is not directly incentivising the building of larger grid scale storage beyond grant-type support. Less than 1GW of grid scale storage capacity is currently in planning.

The government’s direction of travel and general consensus seems to be for gas-fired power stations to fill the gap left by retiring coal plants. Existing gas-fired plants may suffice to cover half of the generation shortfall should combined current coal and nuclear capacities fall, but the remaining gap must be met by new power plants if Britain’s old coal plants continue to close.

New super-efficient coal plants remain an option but look politically unlikely. The more politically palatable carbon capture equipped coal-fired power stations are still not commercially proven and would require significant investment in new infrastructure. From a strategic view, new super efficient coal plants should be part of the mix. However, no-one is forecasting coal new-build of any significant quantity.