Following the credit crash in 2008, it was significant how many debt-riven banks decided to refocus on their home markets; many overseas operations were prematurely sold. With four of the UK’s big six integrated energy companies overseas-owned, there is real concern that a similar scenario could hit the energy sector.

After all, the macro-economic factors are lousy: dire spark spreads; incessant government intervention and political uncertainty, manifested by the Miliband price freeze pledge; and the Scottish referendum.

For Eon, RWE and Iberdrola, returns from their UK investments remain profoundly disappointing, although, in EDF’s case, 2013 output from its existing UK nuclear plants was the highest for eight years.

Neither are the UK duo, Centrica and SSE, exactly happy. Both have effectively deferred any major investment decisions until after the next general election in May 2015.

While it is accepted that energy network prices are subject to periodic price reviews, it has been the generation sector that has recently caused real grief for several big six companies, with low usage and totally inadequate spark spreads. Inevitably, given this scenario – and little confidence that it will change materially for some years – the question is raised ‘“why bother with the UK?”

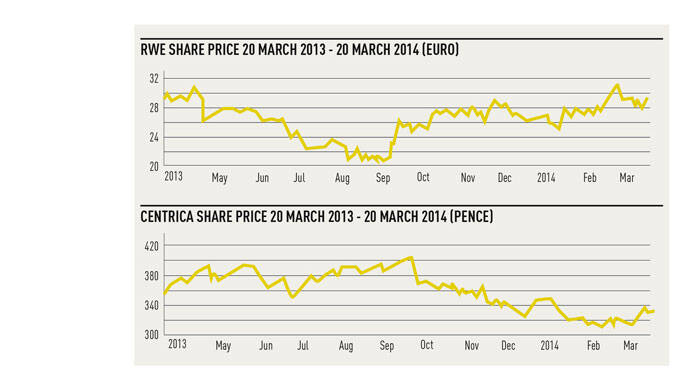

For both German companies, especially RWE, this issue is particularly relevant, since its home market – once a haven of safe, long-term returns – has been turned on its head by the sudden political decision to phase out all nuclear plant by 2022. Furthermore, the premature closure of several coal-fired plants, on environmental grounds, leaves both companies severely exposed.

Modest though it may be, RWE’s UK conventional power generation portfolio still chalked up a €76 million (£63 million) loss at the operating level in 2013, compared with a €194 million profit in 2012. Once the interest element is stripped out, the underlying losses are even higher, although RWE did report a €290 million operating profit on its UK supply operations.

Against this background, RWE’s entire modus vivendi is under review. Whether this culminates in either a lower profile in (or an exit from) the UK remains to be seen. There are few obvious buyers for the Npower business.

Eon does at least have a valuable portfolio of international activities beyond Germany and the UK. As its net debt soared some years ago, there was a real fear that the company had overextended itself, especially in Russia. Its reduction is now paramount.

Eon’s recent 2013 figures confirmed an Ebitda (earnings before interest, tax, depreciation and amortisation) of €9.3 billion, an underlying fall of around 10 per cent on 2012: its mid-range forecast for this year is €8.3 billion. As expected, far lower generation returns are mainly responsible for this shortfall. With the absence of free carbon emissions rights, last year’s Ebitda from steam-fired plants was down by 53 per cent. The comparable CCGT figure was a depressing 64 per cent lower.

Whether Eon’s hitherto resolute commitment to UK energy abides is uncertain. There are many alternative uses for its capital, notably in markets where economic growth is high and politics less capricious.

Judging by its recent strategy update, Iberdrola’s commitment to the UK remains robust, or at least to Scotland should September’s referendum go in favour of independence. Chief executive Ignacio Galan confirmed that no less than 41 per cent of Iberdrola’s expected €9.6 billion net 2014/16 investment budget was earmarked for the UK – a seemingly unequivocal endorsement. He did indicate, though, that new gas-fired generation investment remained on hold until the market recovered.

Given that Iberdrola’s UK generation and supply returns in 2013 were down 11 per cent at €320 million, this caution is understandable. Indeed, the generation segment was effectively loss making. Even so, there remains the possibility that Iberdrola could sell part of its electricity distribution operations if a compelling need to reduce its debt suddenly arose.

After years of negotiation to build a new nuclear plant at Hinkley Point C – with the infamous inflation-adjusted £92.50 per MWh strike price – EDF is hardly likely to run for the hills. However, there is one serious reservation. The EU authorities are carefully scrutinising the massively subsidised price, and substantive contractual changes may well be prescribed.

Indeed, the necessary financial changes could be a deal-breaker. After all, nuclear power is hardly a new generation technology. If the Hinkley Point C project does end in tears, EDF’s raison d’etre for its UK operations become less compelling, although its existing nuclear plants are still throwing off plenty of cash.

While there is minimal likelihood of Centrica exiting the UK in its entirety, an increasing share of its investment may be directed overseas. After all, the company reported a whopping £133 million loss on its CCGT plants over 2013 and, having opted out of the Race Bank project, it is now more discerning about its renewable investments.

On a worse case scenario, Centrica could face a split up of its core UK gas business: the UK regulatory authorities are already on the case. The precedent of the privatised BAA is a real worry as its owners were progressively stripped of Gatwick, Stansted and Edinburgh airports – aside from Heathrow, the mainstay of its business.

In any event, Centrica’s focus is increasingly on oil and gas assets, whether in the North Sea or further afield.

And, despite some disappointing returns in 2013, further North America acquisitions are anticipated. In time, Centrica will expect to emulate Hanson by being “big over here and big over there”.

For almost a generation, SSE has focused almost exclusively on the British Isles – this scenario is unlikely to change. But whether its head office remains in Scotland if the Scottish electorate votes to secede from the UK in September is a different matter.

Unlike Standard Life, SSE remains tight-lipped on the issue, but investors will be concerned about the durability of renewable energy payments if Scotland goes its own way. In any event, SSE is currently not short of challenges within the energy sector, ranging from depressed spark spreads to ongoing distribution reviews.

In summary, of the overseas-owned big six energy companies, RWE’s entire strategy is effectively under review, while Eon has many alternative investment opportunities around the world.

EDF’s UK future seems tied into any developments surrounding Hinkley Point C, while Iberdrola is firm in its UK commitment – at least for now.

Interesting times lie ahead.