Each year, PwC’s Low Carbon Economy Index tracks G20 countries’ progress in reducing the carbon intensity of their economy. In short, this is the energy-related greenhouse gas emissions per million dollars of gross domestic product (GDP).

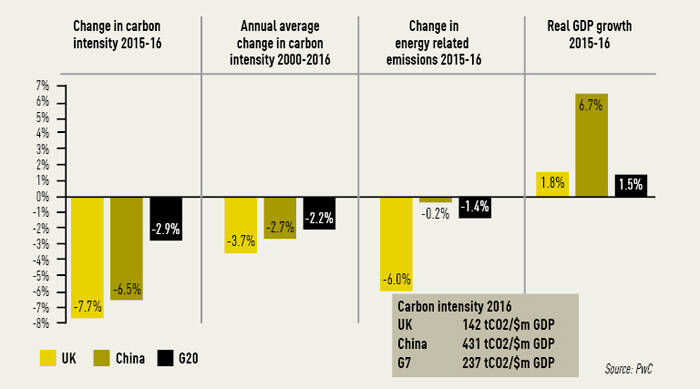

For the UK, our latest initial analysis has delivered some rather remarkable news – a decarbonisation rate of 7.7 per cent during 2016. To put this in context, this is almost three times the global average and in line with the 6.3 per cent annual global reduction required to limit warming to 2 degrees.

This was driven primarily by a 6 per cent drop in energy-related emissions – due to a switch from coal to gas power generation. But steady GDP growth of 1.8 per cent has helped too. The UK power and utilities sector, as the principal consumers of coal and natural gas, have played a key role in this impressive feat.

While Brexit has not affected the UK’s position as a low carbon leader, some uncertainty remains around the UK’s participation in the EU Emissions Trading System (EU ETS), which could severely disrupt that market. However, the UK’s carbon price floor will continue to drive energy generation investment towards lower carbon options.

Understanding the UK’s performance to date

The UK has outperformed the G20 in 2016 on decarbonisation, with China’s 6.5 per cent decarbonisation rate coming closest to the UK’s 7.7 per cent annual reduction. This is not a one-off; our analysis shows that the UK has the highest average decarbonisation rate (3.7 per cent) since 2000. This is better than the average reductions needed by countries to meet their national targets under the 2015 Paris Agreement. So what is helping to drive this performance?

We have seen gas imports increase by 7 per cent and domestic production by 2 per cent. Meanwhile, three major coal-fired plants shut down in 2016 with coal now representing just 7 per cent of UK’s energy consumption, down from 23 per cent in 2012. Policy has played a crucial role in this trend, particularly EU measures to tackle pollution from large combustion plants, but also long-term government plans to close all coal power stations by 2025.

Total energy consumption also fell by 2 per cent in 2016. This was the result of efficiency improvements, despite demand for heating as a result of cooler temperatures. While solar consumption increased by 36 per cent in 2016 and exceeded coal between April and September 2016, progress in other low-carbon energy sources has been modest. Hydro and wind power consumption fell slightly, due in part to low rainfall and wind speeds respectively.

So, can the UK maintain its position as a climate leader into the future? The relatively quick-win transition away from coal which has enabled the UK to rapidly cut emissions is now almost complete. Increasing the share of renewables in the energy mix or further efficiency improvements could help sustain the UK’s impressive decarbonisation performance. Market forces are already driving these trends globally, but ambitious policy and industry engagement in the immediate term could accelerate them further in the UK.

A recent report by the Energy & Climate Intelligence Unit argues that EU-led energy efficiency regulations have played a large part in UK residential energy demand falling by nearly one-fifth from 1990 to 2014. If Britain is to set its own standards for appliance efficiency it will need to replicate or improve on the EU’s regulation to maintain momentum. The UK will also have to focus on other parts of the energy system. The low-carbon transition offers opportunities: electricity demand could double as it replaces natural gas for heat and transport fuel. But this transition will not be easy.

Creating a clear and focused regulatory framework is a challenge for governments not just in the UK, but across Europe. So far we have seen partial commitment to regulation and partial commitment to increasing competition. The current lack of clarity creates uncertainty among investors and utilities. Policymakers must therefore increase dialogue within the sector. This is essential to ensure there is competition to drive technology and business model innovation while providing the strong carbon pricing signals needed to deliver the low carbon transition.

Let us hope the government’s forthcoming clean growth plan provides the vision and clarity investors, utilities and consumers want and need on these matters.