The capacity margin is expected to be only around 5 per cent this winter, compared to the 10-15 per cent generally considered to be sufficient. National Grid issued a warning last month to procure additional resources in response to the threat of such capacity shortages. Historically, energy prices have spiked during periods of short supply. And the Financial Times recently reported that dirty and inefficient diesel backup generators are sometimes being relied upon in these situations.

One potential solution to this problem is demand response (DR). By giving customers incentives to reduce their electricity consumption during times of capacity shortages or high prices, DR lessens the strain on the system. This provides customers with bill savings opportunities, improves system reliability and reduces the need for new fossil generation resources.

DR is allowed to participate in the UK’s Short Term Operating Reserve (STOR) market and the Capacity Auctions. DR represented 7 per cent of the reserve capacity procured for the 2014/15 winter season, although roughly two-thirds of this is provided by backup diesel generators rather than a reflecting a true net reduction in consumption. DR represented only around 0.4 per cent of the capacity procured in the 2014 Capacity Market Auction. Efforts are underway to remove existing barriers to greater DR adoption in the UK. For example, industry stakeholders are currently working to more fully integrate DR into the STOR and capacity markets and to introduce half-hourly settlement for smaller consumers.

But how well do we understand the overall potential for DR in the UK market? A necessary and potentially overlooked first step is to carefully understand the size, cost, and operational capability of any DR resource. Commonly referred to as a “DR potential study,” this type of analysis has served as the foundation for successful DR initiatives around the world. In the U.S., for instance, the Federal Energy Regulatory Commission (FERC) conducted a state-by-state assessment of DR potential in 2009, finding that peak load could be reduced by up to 20 per cent of through new DR initiatives. This was followed by the development of a National Action Plan for Demand Response in 2010. DR has grown at an average rate of 20 per cent per year in the U.S., and much of this growth has been in wholesale electricity markets that are similar in many ways to the UK’s STOR and capacity markets. And while some DR in the U.S. focuses on residential cooling load, which is limited in the UK, the majority of DR capability in the United States comes from commercial and industrial facilities with similarities to those in the UK.

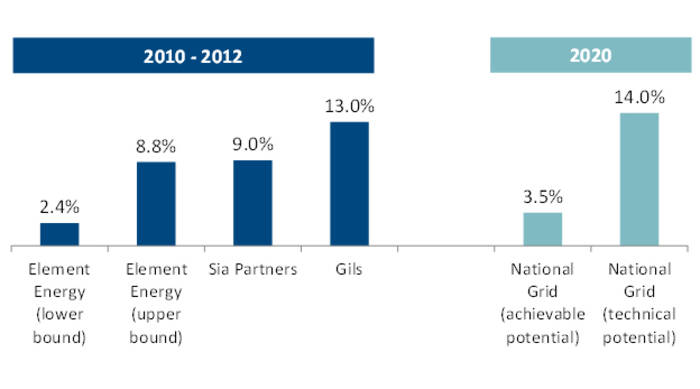

Several studies have explored DR potential in the UK over the past several years, estimating broadly that between 2 per cent and 14 per cent of UK peak load could be reduced through DR. But many unanswered questions remain. What is the likely cost of obtaining meaningful load reductions? To what extent can DR go beyond peak demand reductions to address the emerging need for around-the-clock flexibility caused by increasing levels of production from variable renewable energy sources such as on- and off-shore wind and solar PV? What are the barriers to broader DR adoption? And what are realistic estimates of potential, accounting for customer acceptance?

As stakeholders in the UK power market address these foundational issues, new studies and analysis are needed. For instance, while a single point estimate of DR potential is a useful analytical starting point, it does not capture important details about available DR resources. The development of a DR “supply curve” will provide new insights. Each possible DR program has a different cost, load reduction potential, and operational characteristics, and participation will vary depending on the financial incentive offered. A supply curve highlights the “low hanging fruit” among DR resources and facilitates more robust cost-effectiveness analysis.

It will also be important to account for the impact of emerging DR programs. DR potential studies often focus on “conventional” programs such as interruptible tariffs for large industrial customers. But emerging DR options, such as Behavioural DR, “Bring Your Own Thermostat” programs, smart appliances, electric vehicle charging load control, and smart water heating load control could provide new system benefits. The UK-wide smart meter rollout already underway will provide opportunities to offer a new wave of innovative programs to customers.

The role of tariffs in the DR portfolio should also be explored. More than 40 retail electricity pricing pilots conducted around the world over the past dozen years have found that time-varying rate designs are effective tools for facilitating reductions in peak electricity demand. An important consideration for a competitive retail market like that of the UK will be determining how to encourage the provision and adoption of these rates. A related question is which tariff designs could be achieved with the current settlement system, and which tariff designs would require half hourly settlement.

DR has the potential to play an important role in keeping electricity affordable to customers and maintaining reliability as the UK power system continues to experience increasing reliance on cleaner energy resources and evolving market designs. The industry’s ability to address important emerging analytical questions on the “demand side” will influence the effectiveness of new market rules, energy policies, and consumer product offerings.

Ryan Hledik, Jurgen Weiss, and Serena Hesmondhalgh, principals at the Brattle Group