Over the past three years there has been increasing investigation and criticism of the retail energy market. There have been concerns about the level of prices for customers and assorted claims of excessive profits by the large suppliers and of a lack of real competition, demonstrated by the failure of new entrants to succeed.

This hostile environment comes at a critical time for energy retailers, who are simultaneously being asked by policymakers and regulators to introduce universal smart meters and support the Green Deal and other energy-saving initiatives. The overall context is further complicated by the need for the industry as a whole to attract funding for £200 billion of new investment to revamp and decarbonise the UK’s energy infrastructure.

Inevitably, balancing the various challenges of these multiple demands and widespread criticisms has led to tension and frustration within the industry. So where do we go from here? How might regulatory approaches towards retail evolve? And what might all this mean for the future of the retail energy market?

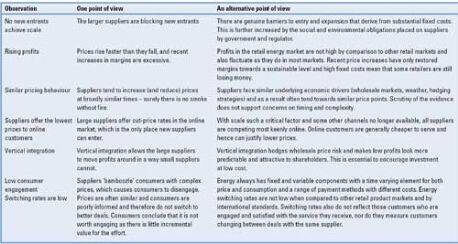

One of the notable features of recent events has been the polarisation of views about the fundamentals. Even where there is agreement on what is being seen – for example, on the limited extent of new entry – there are strong differing opinions as to why this is, to what extent it is in fact a problem and what needs to be done.

As can be seen from the table, it is something of an understatement to say there are differing views on issues facing the industry. What is clear is that it is essential that the regulator puts in place market interventions based on the correct assessment. The implications of getting this wrong are significant for everyone. A recent paper by ex-electricity regulator Stephen Littlechild highlighted both the challenge of obtaining reliable evidence and the risk of substantial unintended consequences if the regulator opts for the wrong approach.

In our opinion, the regulator faces three broad choices. The first option is to focus on continued efforts to sharpen the competitive market. The regulator can continue with the drive to increase price competition between suppliers, increase the liquidity of the wholesale electricity market and improve the transparency of regulatory accounts. However, given the issues about the intrinsic economic characteristics of retail highlighted in the table, there needs to be a strong element of realism in their expected outcomes as well as a clear recognition of the challenges arising from the costs of implementing the new obligations.

Ernst & Young’s analysis of the most recent Ofgem data on segmental costs highlights the importance of fixed costs arising from supply obligations and the critical role of scale. In this environment, less may be more, in that competition between fewer, larger players of similar size could lower aggregate fixed costs for consumers and create stronger competition on service or new products such as energy efficiency.

This logical economic next step, consolidation, would depend on a less confrontational, more rational atmosphere because no investor will commit significant amounts of capital in a business segment with an uncertain future.

The regulator’s second option is to partially regulate the retail market by stealth. The regulator is under immense pressure to do something to “fix” the retail market and has started to introduce measures that partially regulate the prices suppliers can charge. However, as recently recognised by professor Littlechild’s paper, the latest Retail Market Reform proposals risk banning the types of energy tariffs that some consumers most desire and the smaller entrants use to differentiate themselves. Ironically, reducing product differentiation, reducing the ability to cross-sell and increasing price transparency are all likely to make scale even more significant.

The third option is simply to re-regulate the retail market. Although seemingly inconceivable a few years ago, when the emphasis was firmly on the UK’s world-leading rates of retail switching, some are beginning to ask whether re-regulation might now be a better outcome. Certainly, Ofgem faces some difficult choices if the latest round of proposals to reform the market do not deliver the expected results. The consequences of such a decision would be immense, not just for the retail sector, but for the whole energy value-chain and the fundamental approach of investor-led investment in energy infrastructure.

As part of these choices, there is a clear need to re-examine how Ofgem and the market can best balance customer protection, competition, supplier profit, environmental obligations and investor appetite. As part of this, it is essential to develop a clear – and ideally shared – view of what a good retail market looks like. What levels of profit are acceptable and sustainable? What sorts of supplier behaviour are expected and desired? Last, but by no means least, the regulator and market participants need to work together to rebuild the rather bruised consumer confidence in what had previously been viewed as the world’s most successful energy retail market.

https://www.youtube.com/watch?v=R_da5vljGpE

This article first appeared in Utility Week’s print edition of 24 February 2012.

Get Utility Week’s expert news and comment – unique and indispensible – direct to your desk. Sign up for a trial subscription here: http://bit.ly/zzxQxx