Part 1: Having their say?

Utility Week’s Senior Executive Panel on the customer voice in PR14. Karma Ockenden reports

For this the third article in our water customer representation mini-series, Utility Week/Accent quizzed the top industry bosses on our Senior Executive Panel (see box to join) about the customer voice in the upcoming water price review in 2014 (PR14).

Just under one-third (31 per cent) believe current levels of customer involvement – in the form both of customer challenge groups and wider research – are about right. However, half feel there is scope for even more customer engagement. One comments: “I see some organisations are focusing more on an indirect customer engagement via stakeholder groups. I believe there is scope to make more use of low cost channels and social media to engage more widely at a grass roots customer level.”

A residual 13 per cent of executives feel the customer agenda has been driven too hard. One is specifically concerned about potential flaws in surveys where customers are asked to choose between tangible and intangible services. He says: “I’m also worried about risks that the process, and the customer challenge group process, give too much weight to customer views as expressed by these surveys and… that the survey results could be used mechanically to determine outcomes.”

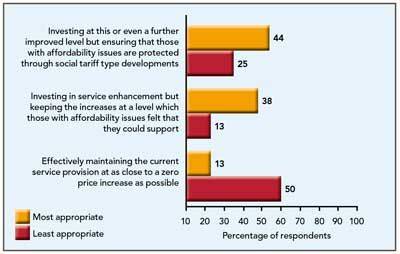

A flip-side risk also emerged, however: that the findings of customer research may be quietly swept under the carpet by companies trying to avoid putting their heads above the regulatory parapet. Asked about appropriate investment levels for PR14 (see bar chart), 44 per cent of panellists advocate investing at the highest level offered by the question (for improved levels of service, with social tariff protection for those with difficulty paying). One respondent explains: “Delaying investment will exacerbate the price issue in the future and all the necessary tools are available today. We need to protect the vulnerable rather than restrain investment to the lowest common denominator or push the problem five years into the future.”

Thirty-eight per cent support investing to enhance service but pegging the increase at a level those with affordability issues could support. Only 13 per cent say it would be better to effectively maintain the current service provision at as close to a zero price increase as possible. One panellist offers: “Service is already high. I would go further and say no increase to price for maintaining the same service. Or with efficiencies back on the table, a small service enhancement for the same price.”

This broadly reflects the customer views emerging from willingness to pay research, though there are question marks over whether some companies will be reluctant to propose increased investment levels in line with this, given that it would be likely to incur greater regulatory challenge (see Accent commentary).

All that said, our executives are not insensitive to the issue of affordability. They were shown a list of four criteria that could be used to assess the worth of a particular business plan: affordability; avoiding investment peak and troughs; “spend to save” – increased investment now to reduce spending in the future; and “spend to protect subsequent generations” by improving environmental performance. Affordability emerges as the most important issue, with 81 per cent support. Nevertheless, the other criteria are also considered important, with support from around two-thirds of respondents.

Other key findings from the survey are:

· Most panellists (63 per cent) believe affordability is given appropriate emphasis in current PR14 arrangements.

· Forty-four per cent support the existing cost-benefit framework underpinning process. The same proportion argue in favour of tweaks to improve it. Only 12 per cent think the approach is fundamentally flawed. One qualifies: “Not a flaw in cost-benefit analysis as such… But there are fundamental flaws in the choice experiment basis of customer surveys. It would be better to link with the Environment Agency’s water framework directive overall benefit valuations and insert these as WTP evidence.”

· Executives were asked how important they thought it was for customers to be given the opportunity to have an input into various stages of the process. Three in four feel inputting into WTP valuations through WTP-type surveys and responding to a proposed 25-year strategic direction is important. Sixty-three per cent mention evaluating alternative five-year business plans, and 56 per cent say responding to the detail of the proposed five-year business plan is important.

Part 2: Zero no hero

Accent’s Rob Sheldon on why the outcomes of PR14 should reflect customer views

There has been a radical transformation in the way customers are involved in developing outcomes for the 2014 price review (PR14) compared with their involvement in the previous regulatory round. According to the findings of Utility Week/Accent’s latest Senior Executive Panel survey, the industry generally affirms the latest arrangements. Customer challenge groups, in particular, are playing a valuable role both in representing customers and developing the creativity and scope of customer research work.

There are critics of the process, of course, and equally those who want to take it further. But overall our experience is that the water industry now a market leader in customer engagement, certainly within regulatory market conditions – and not only in the UK. Five years ago we would have been surprised to hear detailed discussions being held with water company representatives on the relative merits of online groups and panels and on deliberative and co-creation approaches. But that is exactly what is happening.

In addition, this engagement is typically all encompassing, covering domestic and business customers (largely ignored under PR09), as well as internal (staff) and external stakeholders. So is that job done, then? Well, not necessarily, no.

The industry has benefitted from undertaking wholesale reviews of how WTP surveys should be conducted and fed through the process but, by comparison, the business plan validation testing stage has been largely undercooked. It could be argued that this is just as fundamental to the process.

Validation is about choosing between a limited range of potentially competing plans – all of which have satisfied the cost-benefit criteria – and validating that what we have learnt during the earlier stages is robust. Ultimately, a favoured plan will emerge from the understanding gained through this stage.

The buzz word for this stage is “acceptability”. During PR09, attention was largely focused on affordability as a key measure of acceptability and there are strong pressures within the industry to maintain this same focus. Indeed, in some quarters the debate has pretty much centred on what is an acceptable “affordability acceptability” score.

There can be no doubting the need to ensure that the industry is mindful of this key issue, to avoid enhanced levels of water poverty and debt. But there is equally a need to ensure that this agenda does not become the only agenda. The Senior Executive Panel, for instance, saw affordability as a key criterion, but there was also endorsement of other acceptability criteria.

In recent months we have witnessed a number of company discussions that have centred on the desirability of having a (real terms) flat bill outcome for AMP6 (2015-20). Yet customer research across the industry has typically identified two key features: little appetite for industry disinvestment; and an endorsement and a willingness to pay for investment in improved services. Accent has conducted the willingness to pay research for 14 of the water companies, and will be reporting back to Utility Week in a few months on detailed valuations.

Our panel is completely in step with this customer sentiment, with panellists’ most advocated strategy being one of strategic investment leading to a real–terms bill impact but supported by financial help for those who would have difficulty paying for this outcome.

However, as stated above, there is evidence that some companies could be pursuing what they perceive to be the line of least regulatory resistance and only offering customers a flat bill option with some service enhancement and statutory provision (affordable within a flat bill scenario). This is likely to gain customer support on affordability grounds but does not necessarily reflect many customers’ support for improved service that they are willing to pay for.

This exposes this customer engagement phase to some key critiques, including:

· Do customers understand when they are making their assessment what the impact might be for future generations in terms of any potential “catch-up” investment?

· Are they asked about the acceptability of this?

· Equally, would customers support investment which could offer significant environmental benefits for the future but require a real-terms bill impact?

In other words, shouldn’t we be offering a number of detailed options at this stage that have all passed the cost-benefit test and provide the opportunity for customers to assess these against a range of acceptability criteria?

What has become clear from all the work undertaken in the industry in recent months is that customers are not stupid. They are able to understand what the trade-offs are here: that key capital infrastructure and the environment need looking after; but also that they themselves or others in the area might be struggling financially.

Unfortunately, the picture then gets even more complex when companies look to address issues of affordability head on within this process. Many are currently grappling with the issue of social tariffs irrespective of whether their AMP6 proposals will ultimately be delivered within a flat bill context.

This raises a number of issues. First and fundamentally, for much of the public this is not seen as a water company issue but a government issue, and so customers potentially resent having to pay more to cross-subsidise those who are struggling. Second, most customers are not really aware of the current cross-subsidy provision set aside for unpaid bills and, when they are informed about it, resent it. At the same time customers raise the issue of whether this policy could be used to help reduce levels of debt and counteract current levels of cross-subsidy.

Possibly the most difficult issue in this regard emanates from the fact that, if companies seek to take the line of least resistance and offer a flat bill plan, then any bill impact for social tariff outcomes will look disproportionate – a five-year investment plan costing nothing in real terms set alongside the introduction of social tariffs adding £x to the bill. Paying something for nothing is not likely to be an enticing message for many customers.

How different might this be if the message were “we are investing on your behalf in improving the service and protecting future generations and this will cost you £x and on top of that we would like you to think about whether you would also be prepared to help some specific customers that at the moment are in this (defined) level of water poverty”?

It is not easy to evaluate all these issues, but they need to be considered simultaneously because they are interrelated. We only get one significant shot at this every five years and we need to make sure its aim is true.

Rob Sheldon is managing director of Accent

This article first appeared in Utility Week’s print edition of 19th April March 2013.

Get Utility Week’s expert news and comment – unique and indispensible – direct to your desk. Sign up for a trial subscription here: http://bit.ly/zzxQxx